By Kyle Krumlauf – Senior Director, Industry Analytics

After several years of rapid growth and rising adoption, the U.S. electric vehicle (EV) market is entering a more nuanced phase defined less by acceleration alone and more by variability, shifting economics, and downstream impacts across the auto ecosystem.

While EVs continue to represent a relatively small share of the total vehicle population, their influence is expanding quickly in newer vehicle segments, claims activity, and repair dynamics. This report examines the latest trends shaping EV sales, vehicles in operation, claims outcomes, and repair economics – highlighting how the market is evolving and what it may signal for insurers, repairers, and consumers alike.

Sales and Vehicles in Operation

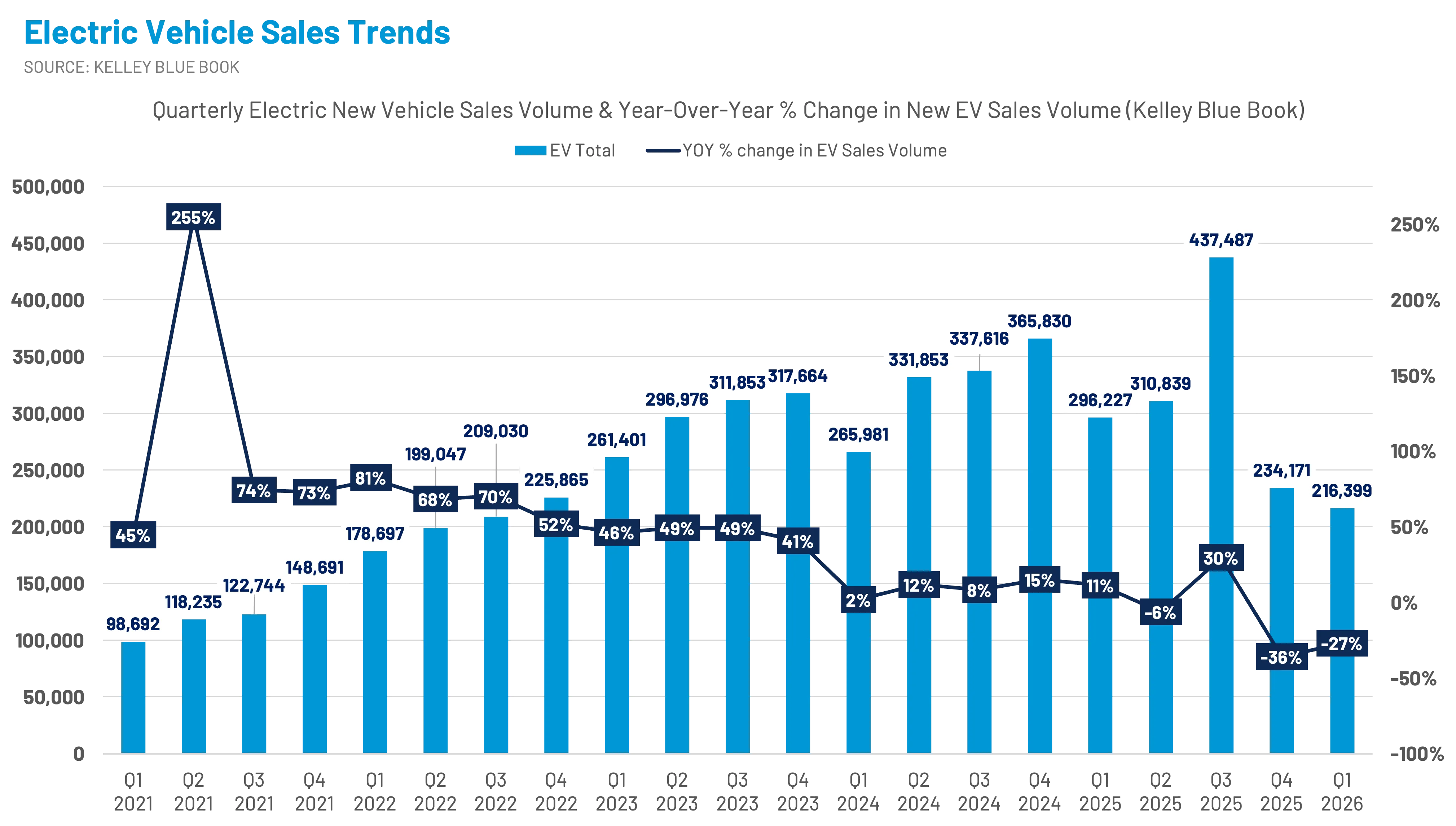

Following the expiration of the Inflation Reduction Act (IRA) tax credits at the end of September 2025, the EV segment experienced a dramatic decline in sales. New EV sales increased by 30% year-over-year in Q3 2025, before falling sharply by 36% in Q4. This downward trend continued into 2026, with Q1 sales down 27% versus 2025, totaling just over 216,000 units—the lowest quarterly volume since Q3 2022.

At their peak in 2024, EVs represented approximately 8.2% of all light vehicle sales in the United States. A 2% decline in EV sales in 2025 reduced that share to 7.9%, even as overall new vehicle sales increased by 2.6%, according to Kelley Blue Book and the Federal Reserve Bank of St. Louis. More recently, EV share fell further to 5.8% of light vehicle sales in both Q4 2025 and Q1 2026.

Leasing continues to play an outsized role in EV adoption. According to Experian, more than 58% of new EVs were leased in 2025, up from nearly 46% in 2024. Although EVs accounted for less than 8% of total new vehicle sales, they represented more than 22% of all new auto leases in 2025. This leasing concentration is expected to drive a significant increase in off-lease EV supply in the coming years: approximately 298,000 units in 2026, rising to 600,000 in 2027 and approaching 795,000 in 2028.

From a vehicles-in-operation (VIO) perspective, EVs still represent a relatively small portion of the total car parc. Of the approximately 296.5 million light-duty vehicles in operation as of Q4 2025 (Experian), about 5.7 million – or 1.9% – are fully electric. By comparison, there are approximately 12.2 million hybrid vehicles (including plug-in hybrids), representing about 4.1% of VIO. Internal combustion engine (ICE) vehicles continue to dominate, accounting for roughly 94% of vehicles in operation, or approximately 278.7 million vehicles spanning decades of model years.

Claims Mix by Fuel Type

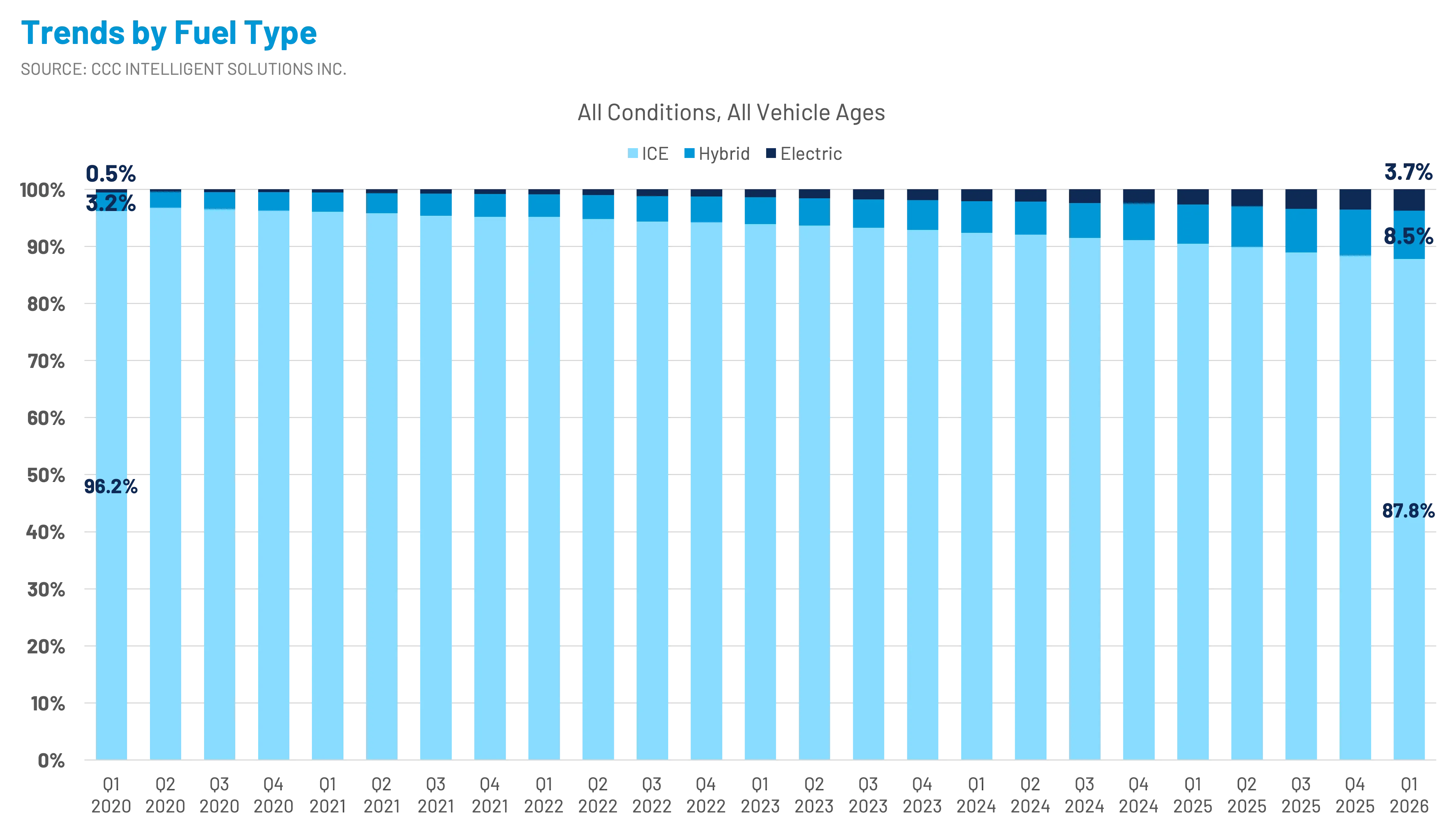

From an auto claims perspective, EVs now represent 3.7% of the claims mix, while hybrids account for 8.5% and combustion engine vehicles for 87.8%.

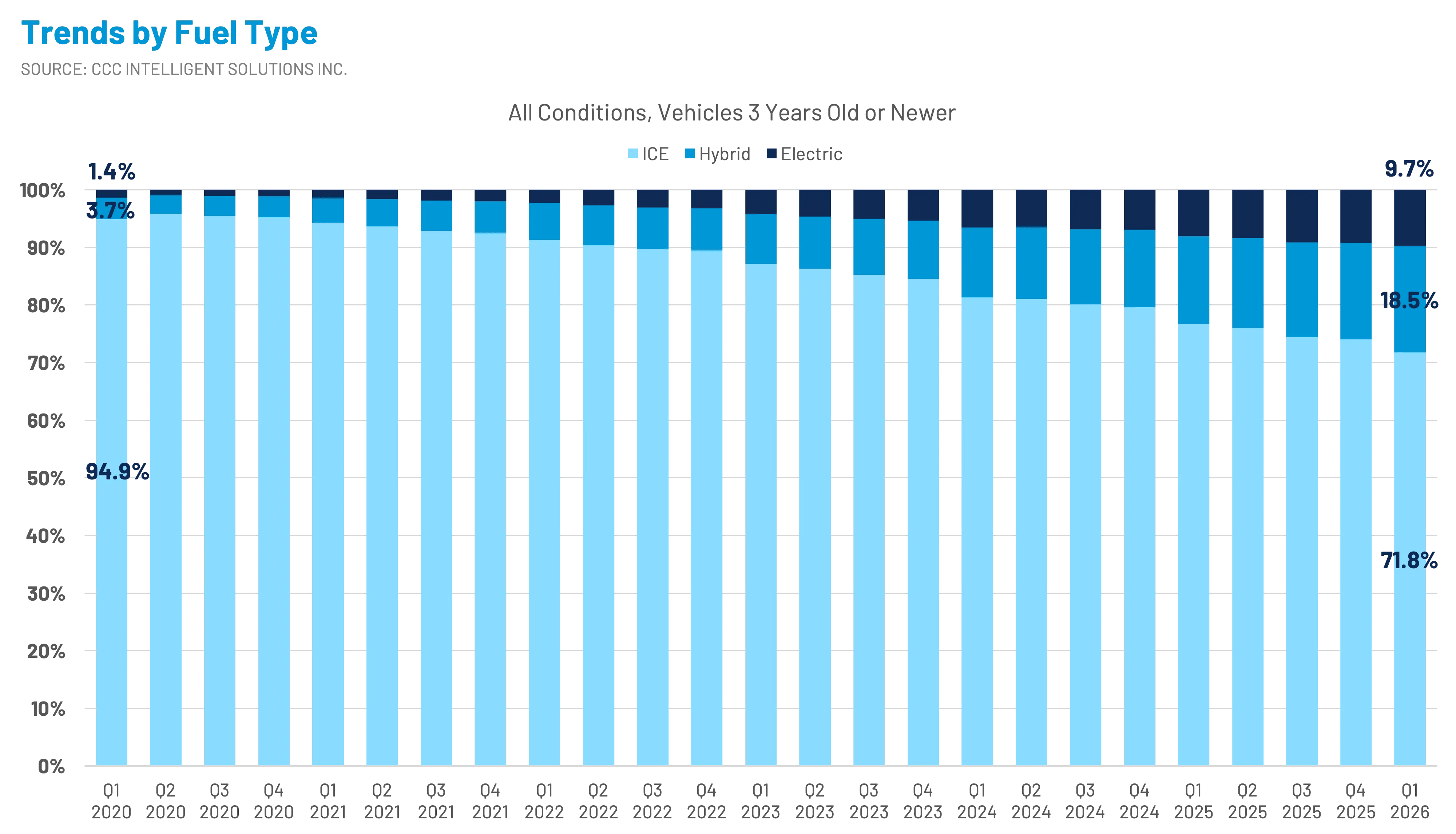

However, this distribution shifts significantly when focusing on newer vehicles. Among vehicles three years old or newer, EVs represent 9.7% of the mix and hybrids 18.5%. Over the same period, the share of combustion engine vehicles in this segment has declined sharply – from nearly 95% in 2020 to less than 72% – illustrating the rapid electrification of the newest portion of the vehicle fleet.

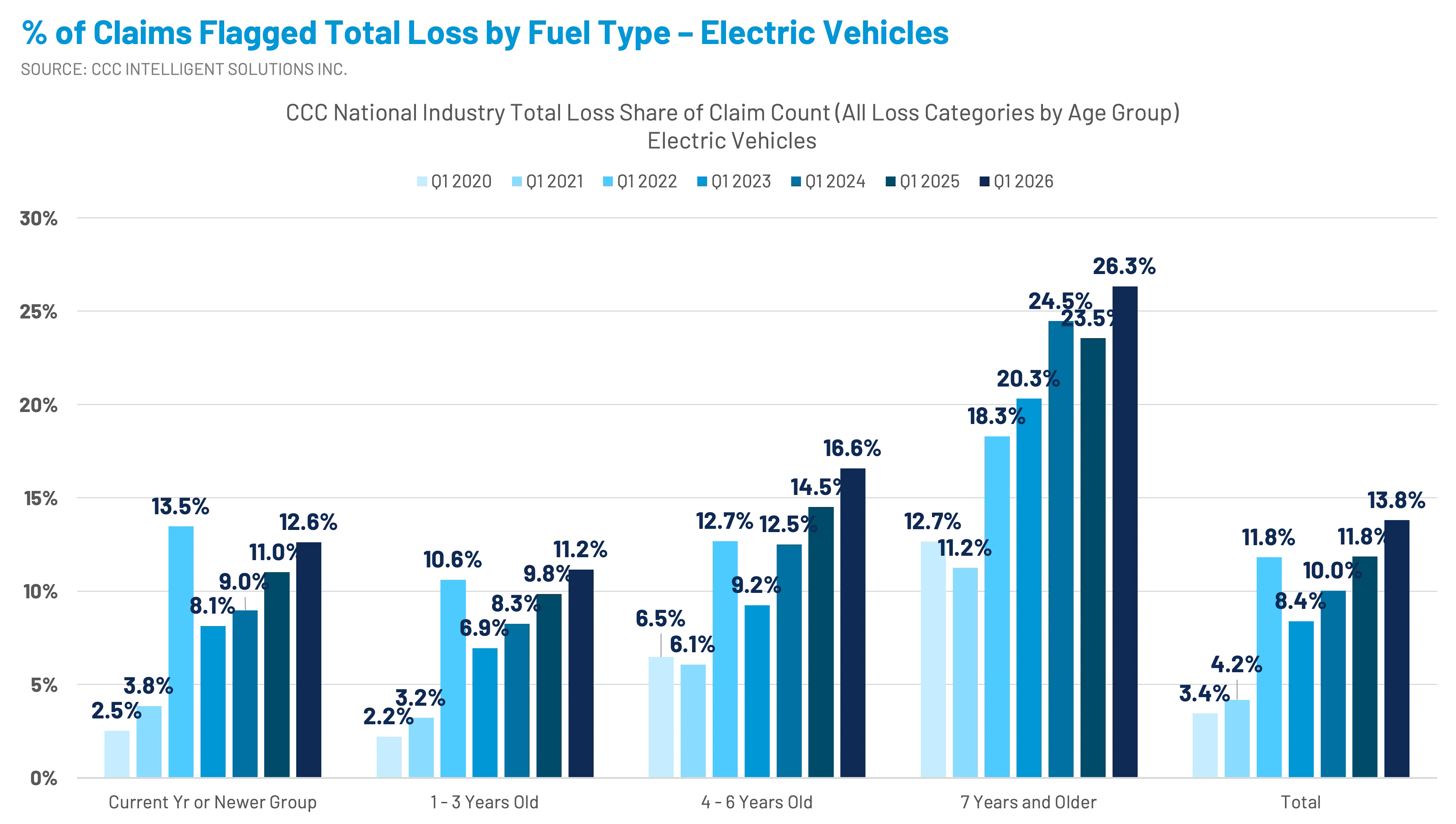

EV Claims: Total Losses

As the EV segment has grown, early attention centered on repairability and repair costs – particularly battery-related concerns. Increasingly, however, the focus is shifting toward the used EV market, vehicle values, and total loss dynamics.

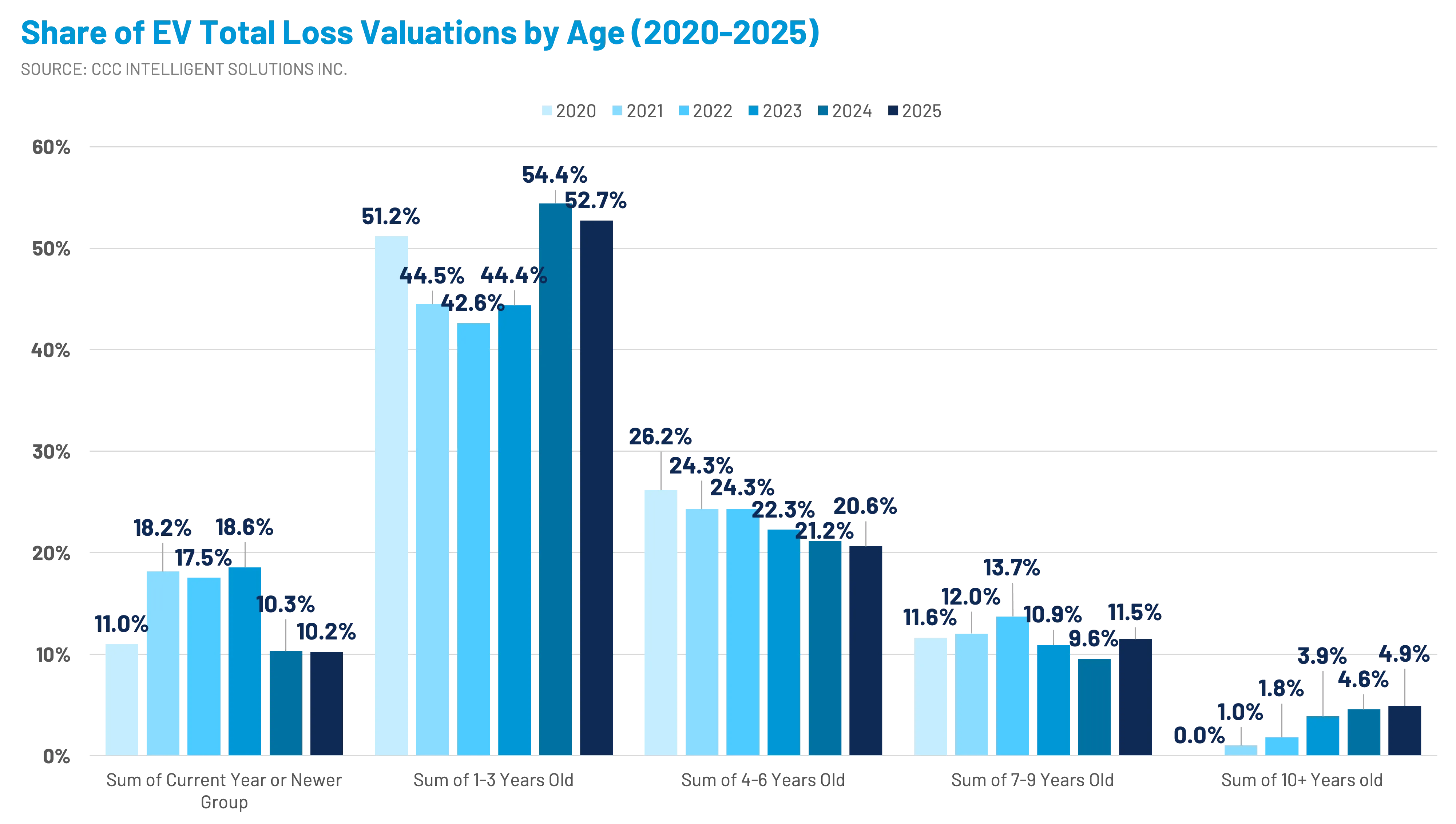

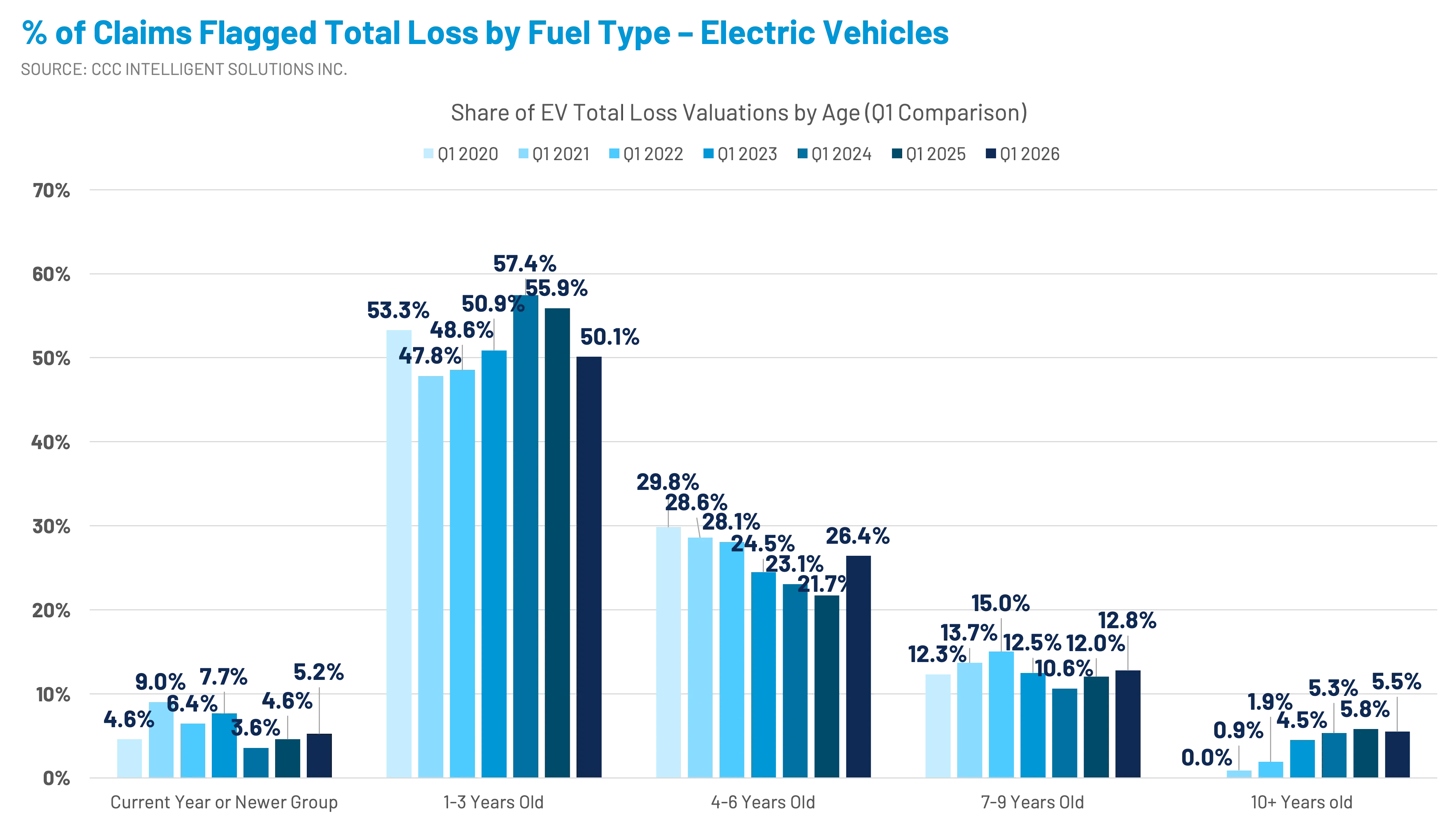

Given the relative newness of EVs, the mix of potential EV total losses (valuations) is heavily skewed toward younger vehicles. In both 2024 and 2025, vehicles aged one to three years represented over half of EV valuations. This stands in contrast to the broader market, where vehicles seven years or older account for more than 70% of all valuations, driven largely by older combustion engine vehicles.

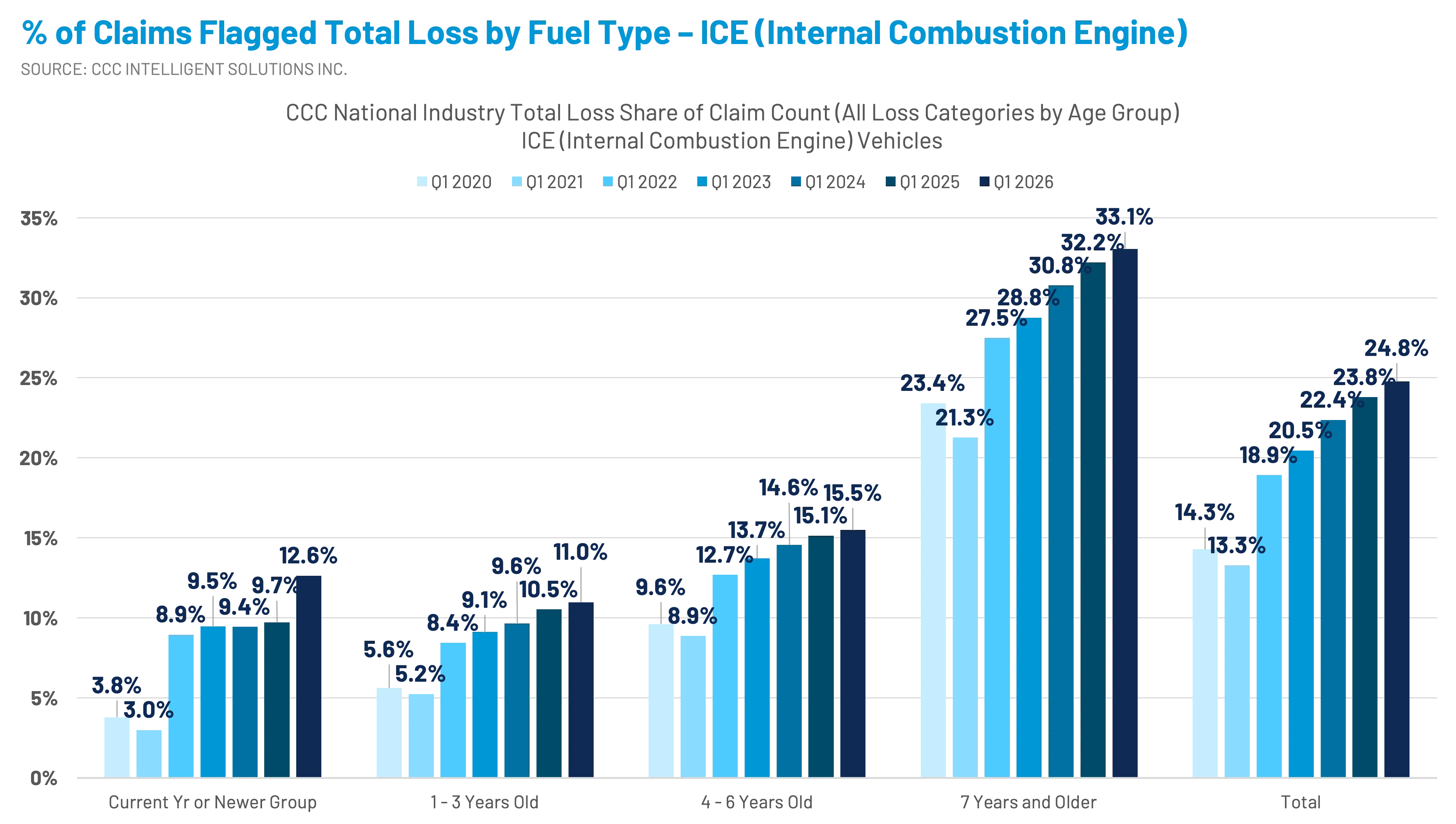

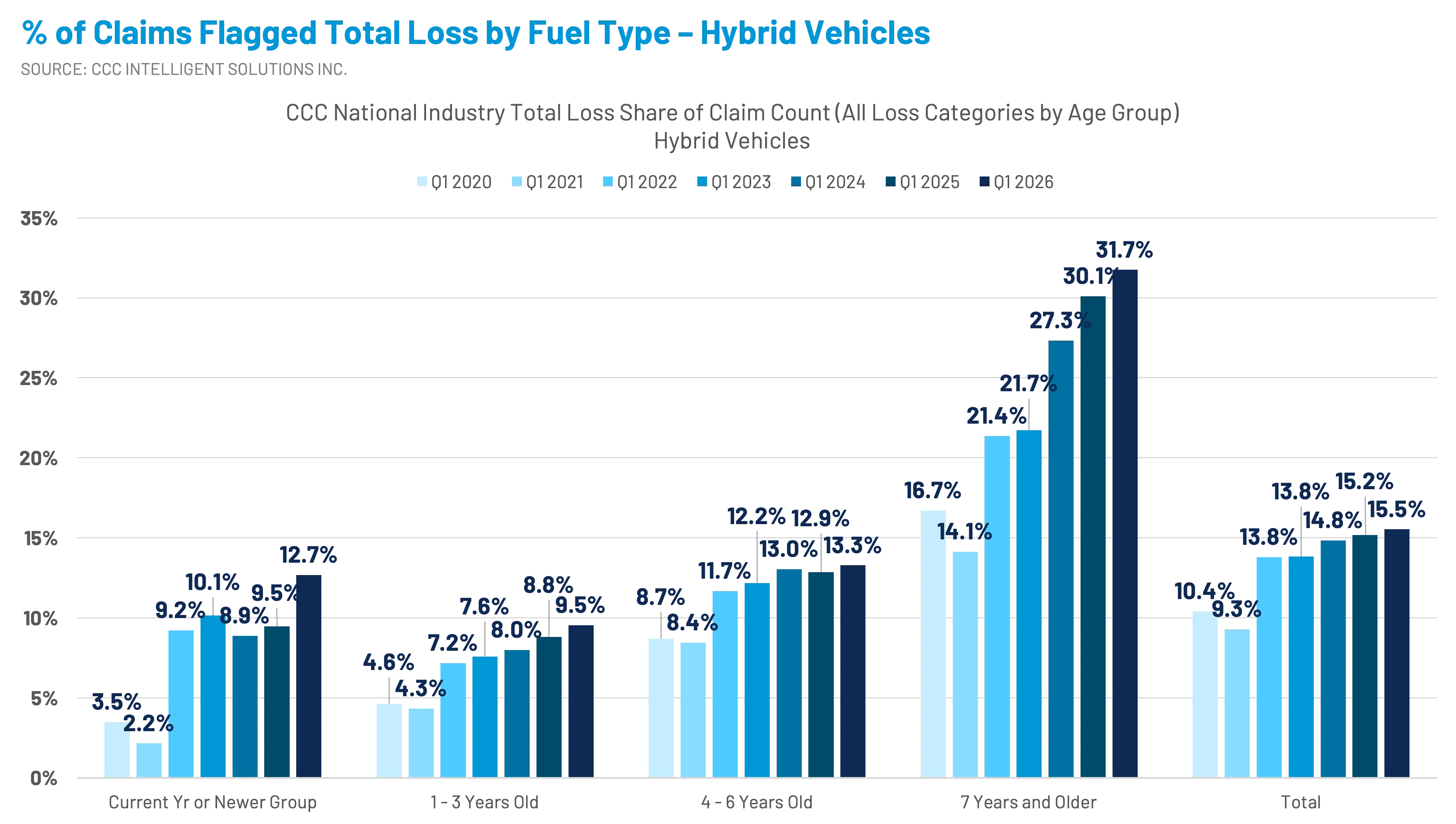

In 2025, 12.7% of EV claims were flagged as total losses, representing an increase of nearly 2 percentage points from 2024. By comparison, the overall industry total loss rate was 23.1%. Combustion engine vehicles, which tend to skew older, experienced a 24.1% total loss rate (up 1.1 percentage points), while hybrid vehicles saw 15.1% of claims flagged as total losses (up 0.1 percentage points).

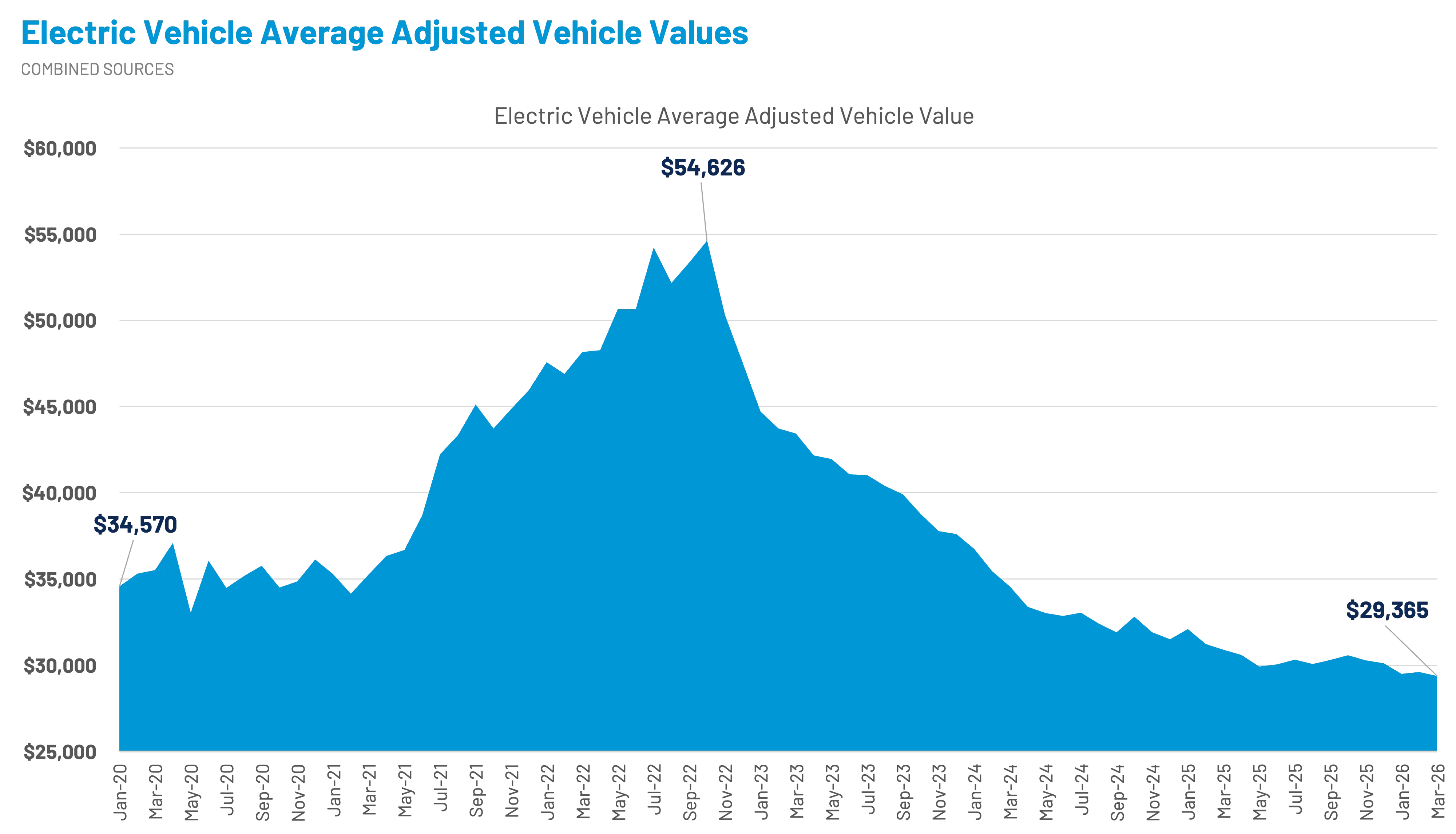

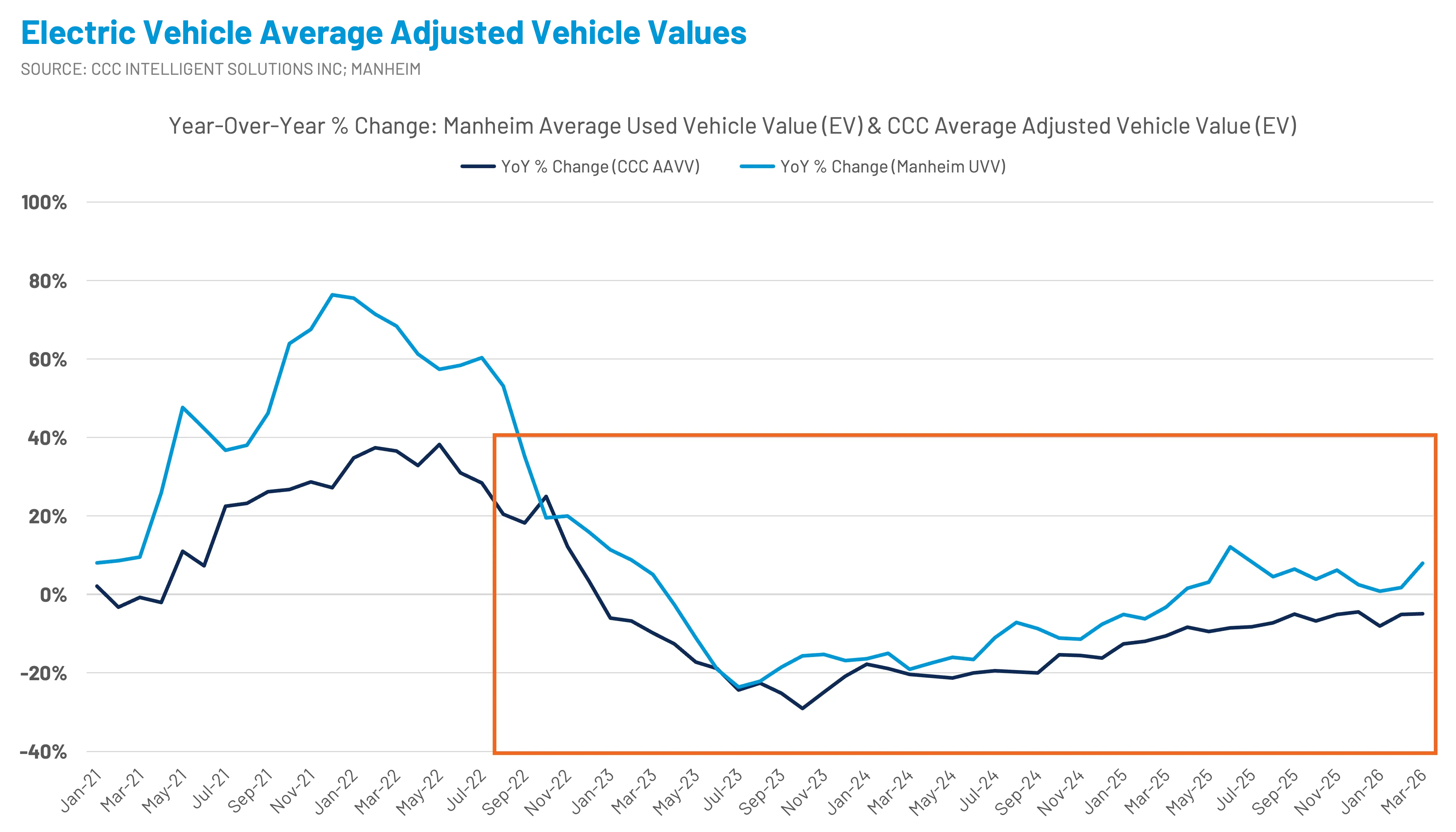

Vehicle values are playing an increasingly important role in these trends. Average adjusted vehicle values (AAVV) for EVs have declined by 46% since October 2022, compared to a 17% decline across the broader industry.

The year-over-year change in AAVV for potential EV total losses has closely tracked the year-over-year change in Manheim’s used vehicle values for EVs following the inflationary period of 2021–2022.

The Manheim Used Vehicle Value Index (UVVI), which typically serves as a leading indicator for used vehicle prices, increased by 6.3% year-over-year as of March 2026. EV-specific values rose by 7.9% over the same period, compared to a 6.0% increase for non-EVs. Cox Automotive estimates that more than 100,000 used EVs were sold in Q1 2026—the second-highest quarterly total on record, behind Q3 2025.

Despite these recent increases, EVs continue to experience above-average depreciation. According to an iSeeCars study, eight of the 25 vehicles with the highest five-year depreciation are EVs, each exceeding 55% depreciation. On average, EVs depreciate by 57.2% over five years—representing an average loss of more than $28,000 relative to MSRP. By comparison, the overall market average is 41.8% (–$16,571), and hybrids average 35.4% depreciation (–$13,010).

From a claims standpoint, this level of depreciation has several implications. It may contribute to an increased share of total losses within the EV segment, influence salvage values, and affect consumer outcomes – particularly where the gap between a vehicle’s value and outstanding loan balance widens. At the same time, declining values may make used EVs more attractive to cost-conscious consumers, particularly as off-lease supply increases, though concerns around battery life, degradation, range, and long-term value retention are likely to persist.

EV Claims: Repair

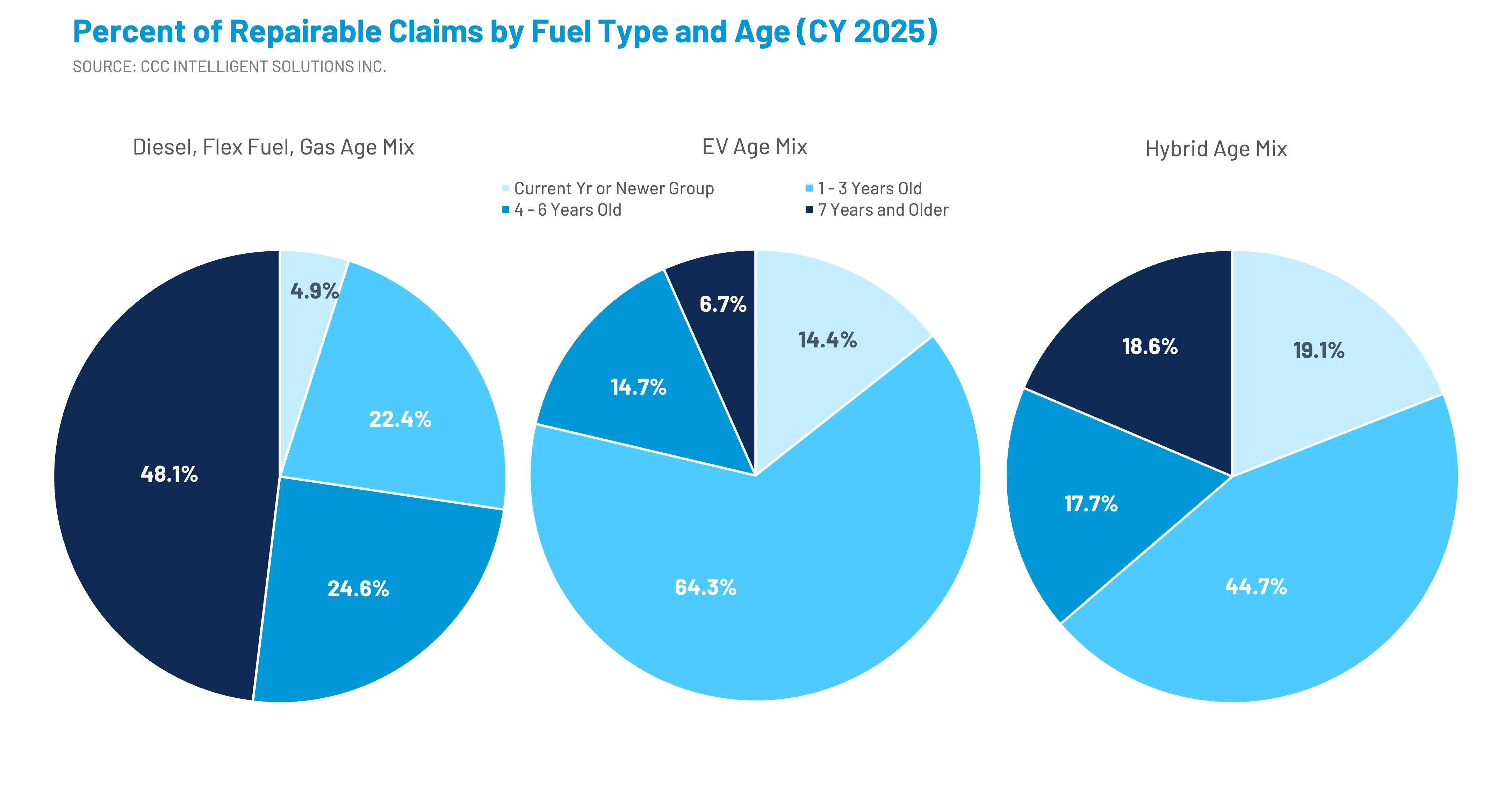

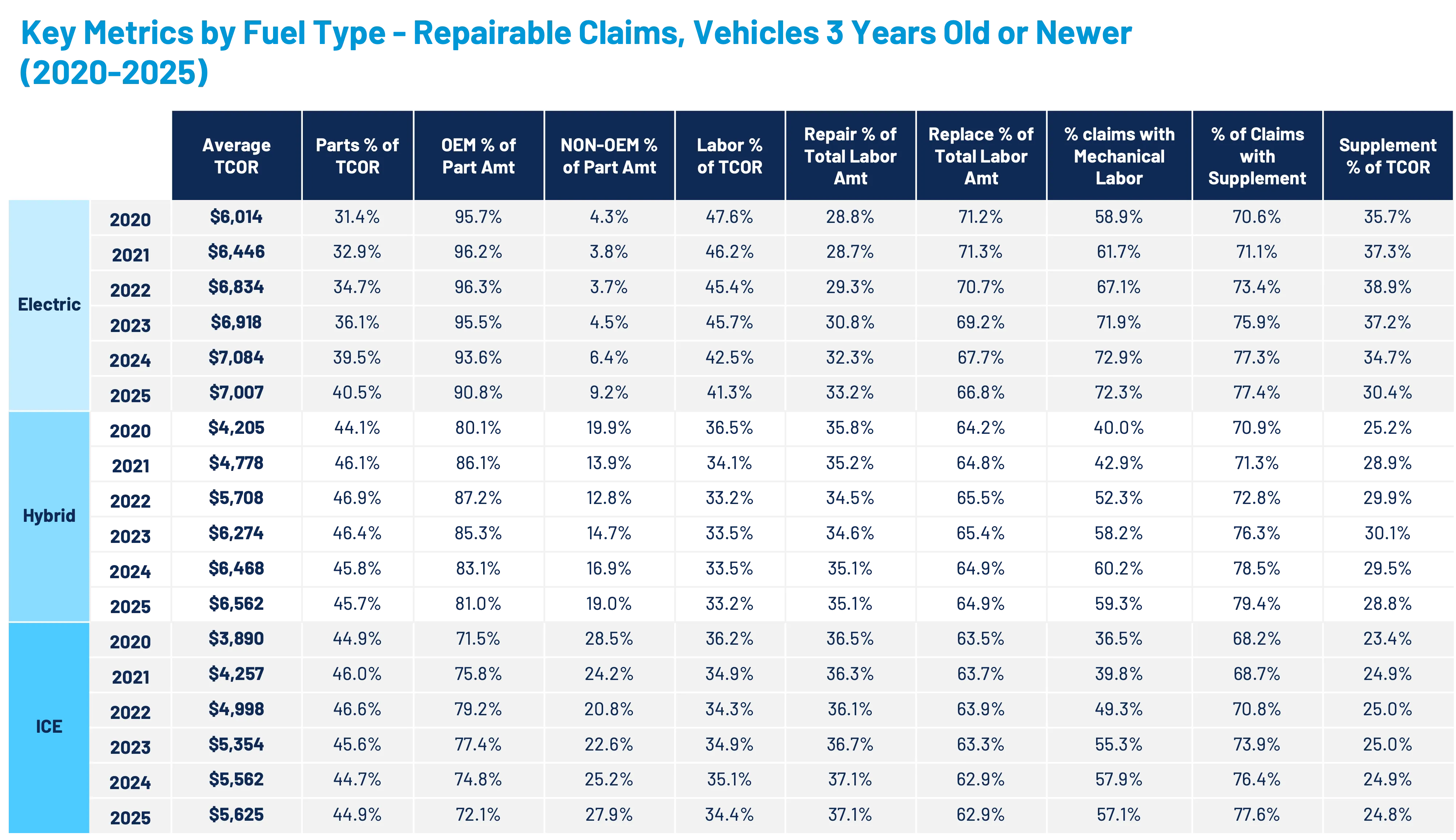

Repairable vehicle claims vary considerably by vehicle age when comparing fuel type. If you might recall from CCC’s Crash Course Q1 2025 report, hybrid and electric new vehicle sales took off in 2021. In other words, the EV segment is very young, especially when compared to the mix of internal combustion engine vehicles.

In 2025, more than 93% of repairable EV claims involved vehicles six years old or newer. For hybrids, vehicles six years or newer accounted for over 81% of repairable claims. In contrast, only just under 52% of repairable claims for combustion engine vehicles fell into this age range.

At the older end of the spectrum, 48.1% of repairable claims for combustion engine vehicles involved vehicles seven years or older. This compares to 18.6% for hybrids and just 6.7% for EVs, further underscoring the relative youth of the EV fleet.

Because of these differences, comparisons of repair costs often focus on vehicles three years old or newer to better align cohorts across fuel types.

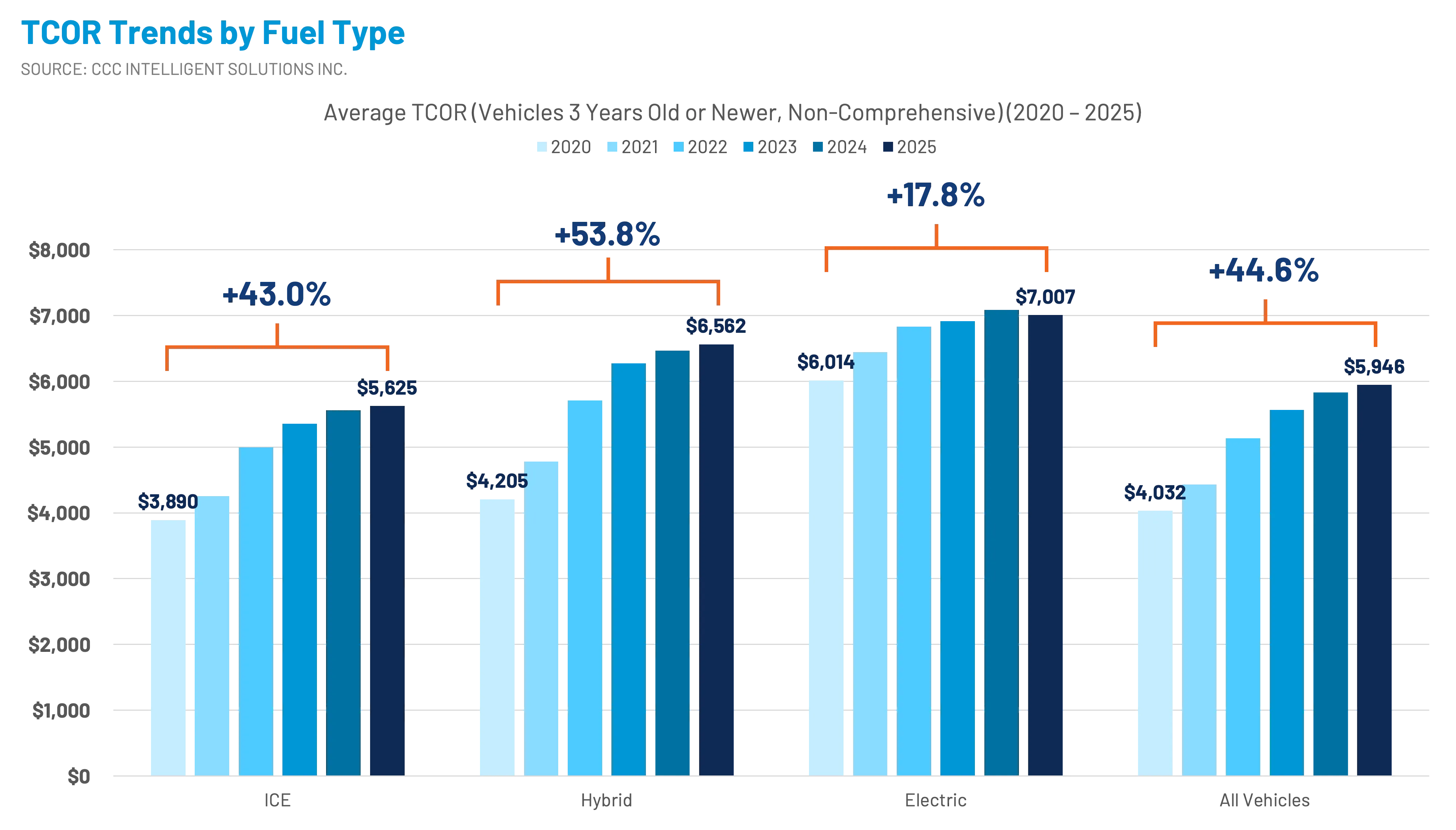

In 2020, the average total cost of repair (TCOR) difference between EVs and hybrids in this age group was $1,809, with EVs costing approximately 43% more to repair. By 2025, that gap had narrowed significantly to $445, with EVs costing only about 7% more than hybrids on average.

This convergence reflects several overlapping factors:

- The average TCOR for hybrid vehicles three years old or newer has increased by nearly 54% since 2020—outpacing other fuel types.

- The increase in EV repair costs slowed in 2023 and 2024 and decreased slightly in 2025.

- Hybrid vehicles have grown in size and incorporate increasingly complex mechanical systems.

- While Tesla continues to lead EV market share (46.2% of sales in 2025 and an estimated 48% of EVs in operation), legacy automakers are gaining share.

- Greater technician familiarity with EV platforms and improved parts availability have helped moderate repair cost growth.

Beneath these averages, however, important differences remain – particularly in labor. While the labor cost gap between EVs and hybrids has narrowed from more than $1,300 per repair to just over $700, EV repairs still require more labor on average. This reflects both higher labor hours and higher labor rates. The difference in labor hours alone has declined from nearly eight additional hours per EV repair in 2020–2021 to fewer than two hours in 2025.

Additionally, more than 70% of EV claims include mechanical labor, compared to approximately 60% for hybrids. As highlighted in CCC’s 2026 Crash Course report, mechanical labor typically carries higher hourly rates, contributing to the remaining cost differential.

In contrast, total parts costs are slightly higher for hybrids than for EVs among vehicles three years old or newer, by approximately $160 per repair.

What to Watch For

Looking ahead, the EV market is being shaped by a series of competing forces. Proposed rollbacks to emissions standards in late 2025 stand in contrast to geopolitical developments – such as conflict with Iran – that have contributed to rising oil prices. These dynamics create a fundamental tension for both automakers and consumers: whether to accelerate or recalibrate EV strategies in the face of economic, regulatory, and energy market uncertainty.

At the same time, the rapid expansion of off-lease EV supply, ongoing depreciation pressures, and evolving consumer perceptions around value and performance will continue to influence demand. Together, these factors suggest that the EV market may experience increased volatility in the near term, even as long-term electrification trends remain intact.

Conclusion

EV sales volatility, shifting residual values, and evolving repair dynamics are introducing new considerations for every stakeholder in the ecosystem. At the same time, EVs are becoming increasingly concentrated in newer vehicles, ensuring their influence on claims, repair, and total loss outcomes will continue to grow.

For insurers, repairers, and industry participants, the challenge is not simply to track EV adoption, but to understand how these intersecting trends – leasing cycles, depreciation, repair convergence, and policy uncertainty – are redefining the economics of the market.