By Kyle Krumlauf – Senior Director, Industry Analytics

In less than a decade, vehicle diagnostics have gone from a niche operational process to critical mainstay in nearly every repair. At the center of this transformation is calibration – the precise resetting of sensors, cameras, and other advanced driver assistance system (ADAS) components included in most modern vehicles.

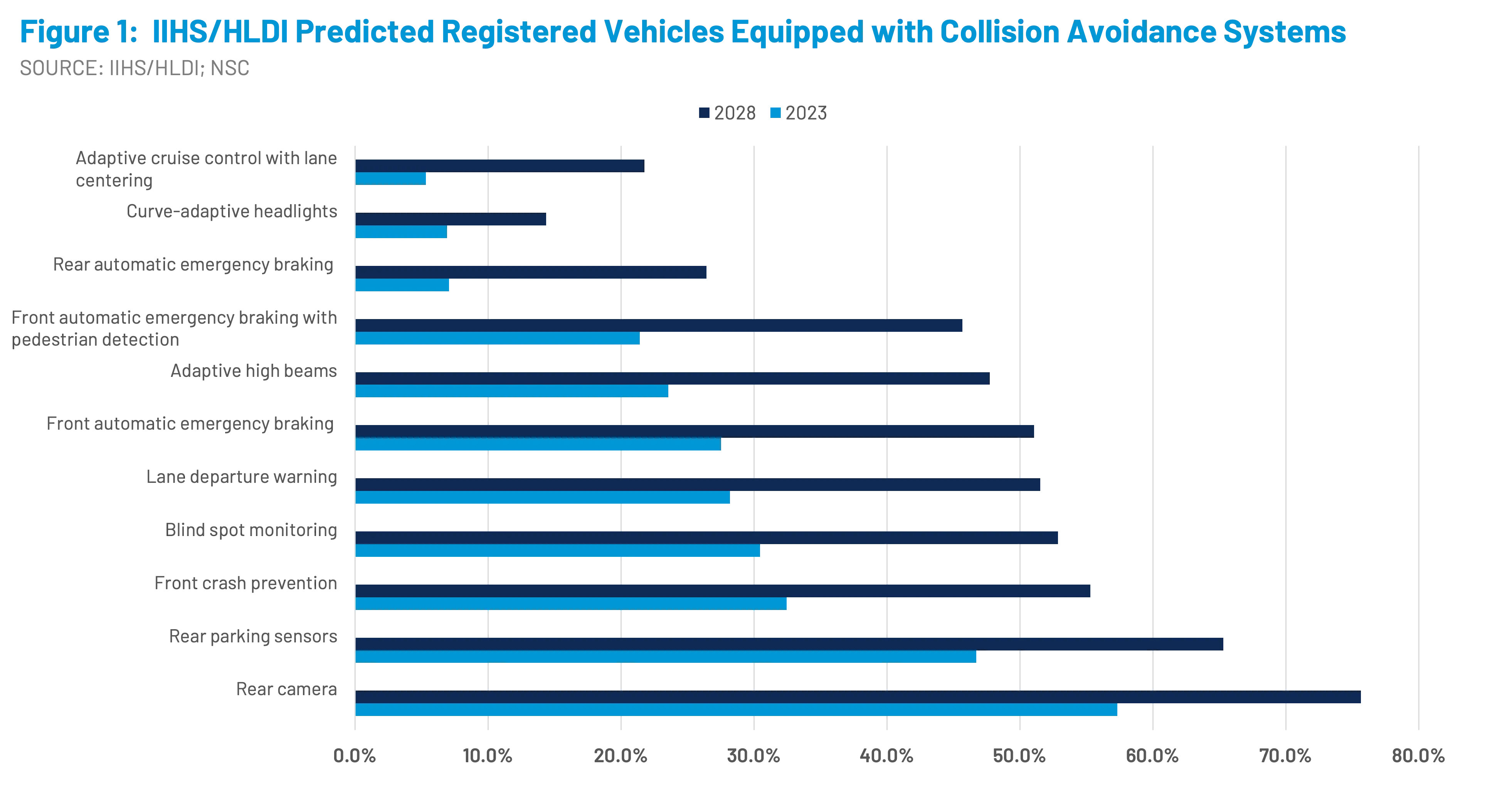

Once considered an infrequent add-on, calibrations have become essential as ADAS technologies spread rapidly through the U.S. car parc. Rear cameras, automatic emergency braking, blind-spot monitoring, and lane departure systems are features that now come standard on most new vehicles and will soon dominate the roads. According to projections by the Highway Loss Data Institute, eight ADAS systems will be present in half or more of registered vehicles by 2029, compared to just three by 2027. (Figure 1)

For collision repairers, auto insurers, and vehicle owners, this shift has fundamentally altered the repair process. Repairs now require not just mechanical and cosmetic fixes but also digital precision to ensure vehicles leave the shop fully functional and safe. This is important, as a misaligned camera or uncalibrated sensor can compromise system performance, exposing drivers to risk and repairers to liability.

CCC data indicates a very clear rise in calibrations. In 2017, only 0.9% of repairable appraisals included a calibration. By 2025, that share had surged to more than 23%, with the growth rate accelerating year over year. In Direct Repair Program (DRP) claims – which are more representative of vehicles that are repaired – nearly one-third of appraisals now include a calibration.

As vehicle complexity has continued to increase and more vehicles require calibration, the percentage of shops that can perform all of the necessary calibration in house hasn’t increased at the same pace to meet growing demand. This is one of the reasons why average calibration fees have nearly doubled in just five years, reaching about $500 per repairable vehicle. And while diagnostic scans are typically captured upfront in the initial estimate (E01), less than half of calibrations appear there. More often, they show up as supplements later in the repair process – adding time, cost, and operational complexity.

This comprehensive look at the current state of calibrations in the U.S. auto repair industry will examine how they're reshaping repair costs, cycle times, and claims dynamics. An in-depth analysis of CCC's historical data – combined with projections from IIHS/HLDI - reveals a clear trajectory: as ADAS proliferates, calibrations will no longer be the exception – they'll be the rule.

The challenge for insurers, repairers, and OEMs is not whether calibrations will become central to the claims and repair ecosystem, but how quickly the industry can adapt to manage their rising prevalence, costs, and complexity.

Historical Evolution of Diagnostics

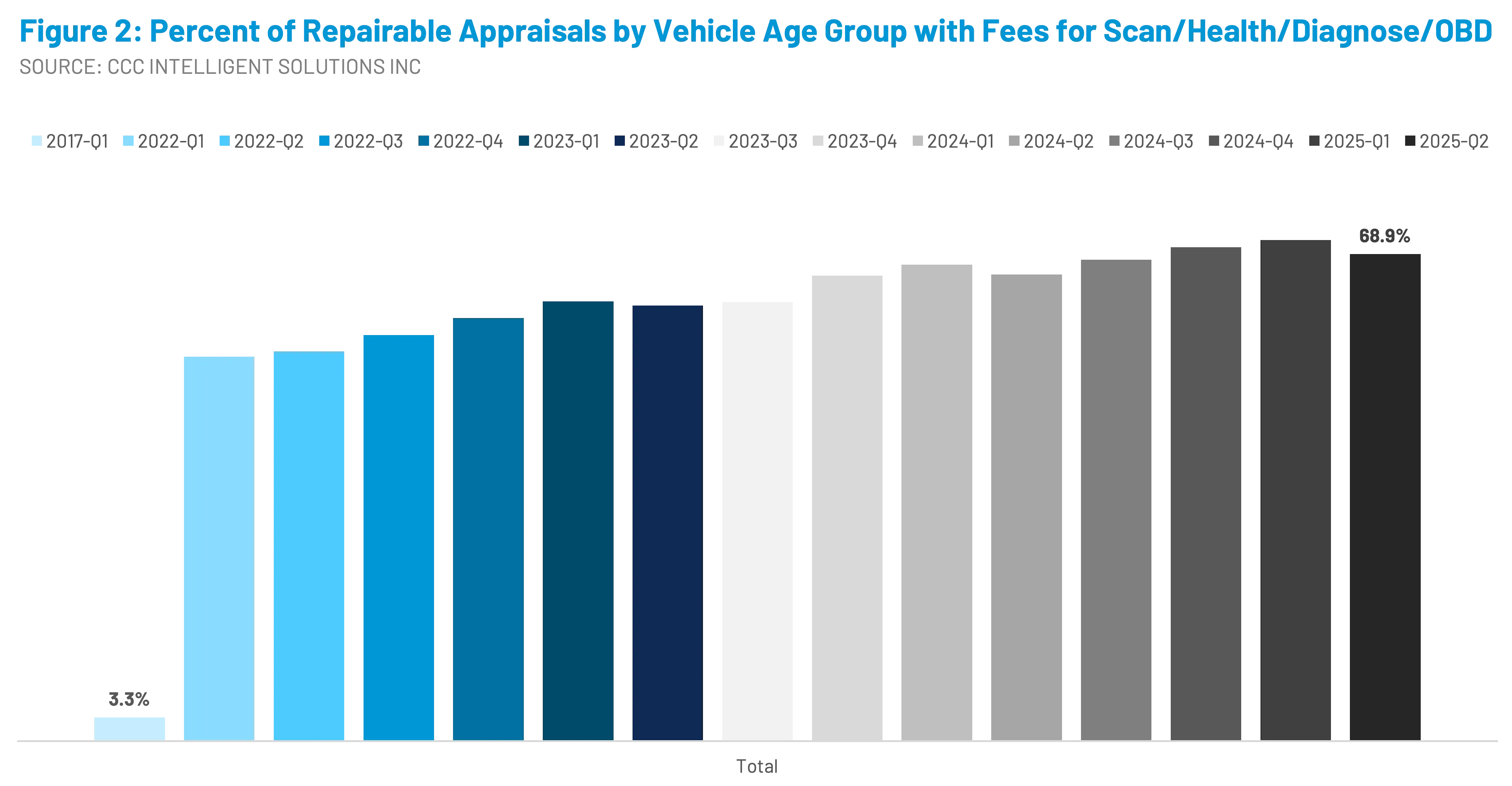

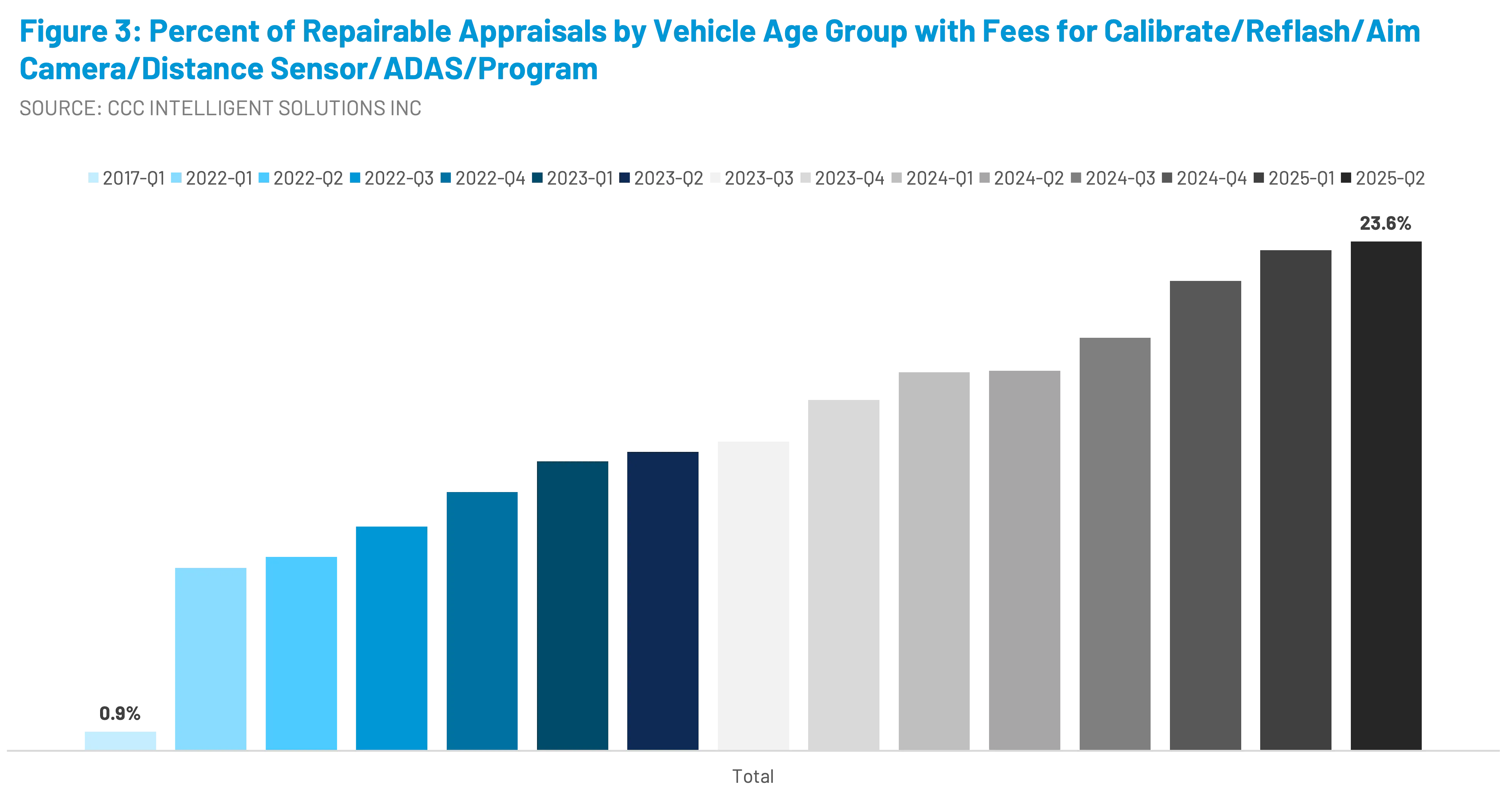

The story of calibrations cannot be told without looking back to when diagnostics first emerged as a regular part of the collision repair process. In 2017, diagnostic scans were only beginning to appear on estimates. At that time, just 3.3% of repairable appraisals included a diagnostic scan, and fewer than 1% (0.9%) included a calibration. (Figures 2 & 3)

This early adoption coincided with the initial wave of ADAS-equipped vehicles entering the market. Rearview cameras, mandated by federal law starting in 2018, provided the first glimpse of how ADAS would reshape vehicle safety. Soon after, front automatic emergency braking and blind-spot monitoring systems began to proliferate, gradually shifting the requirements for proper repairs.

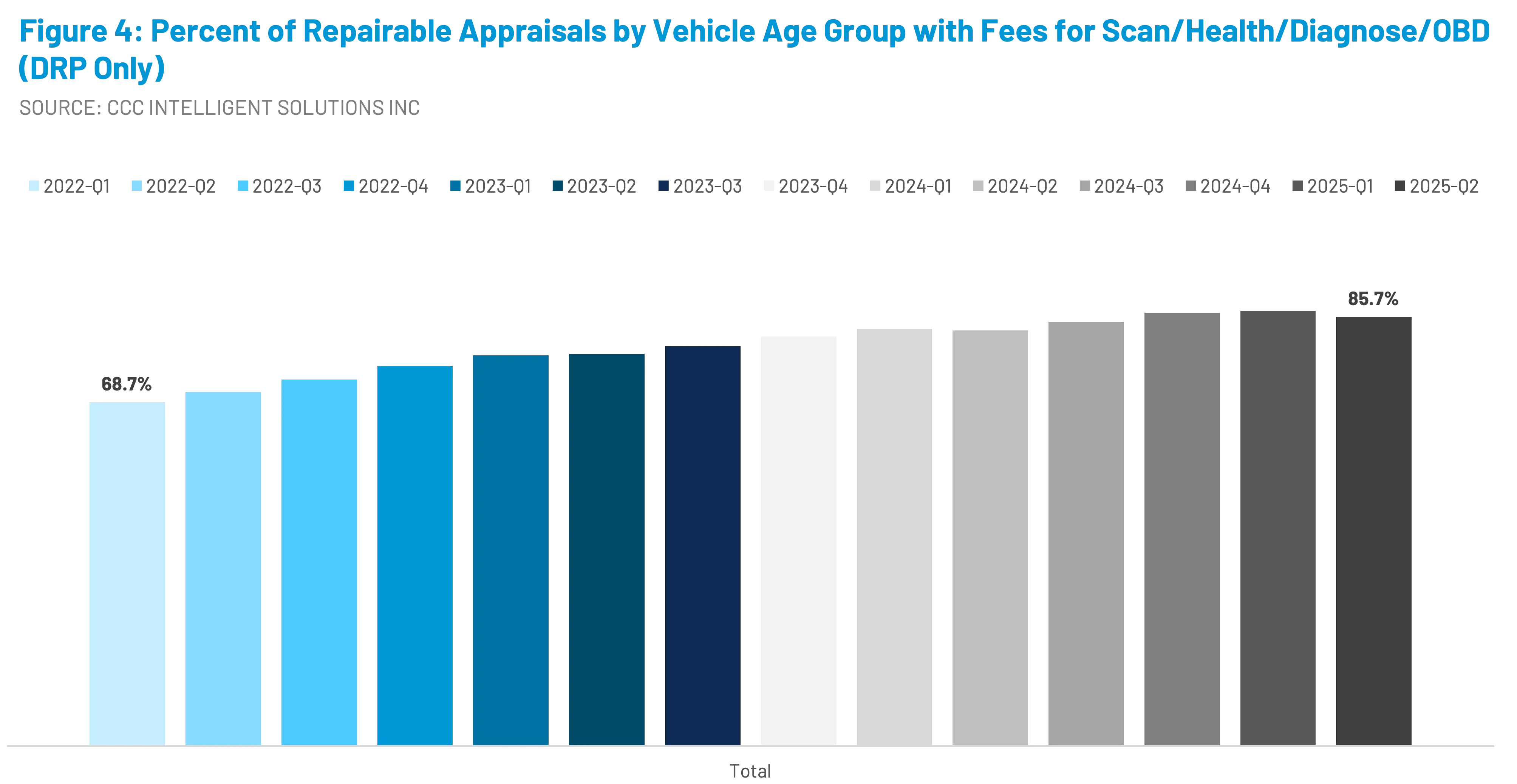

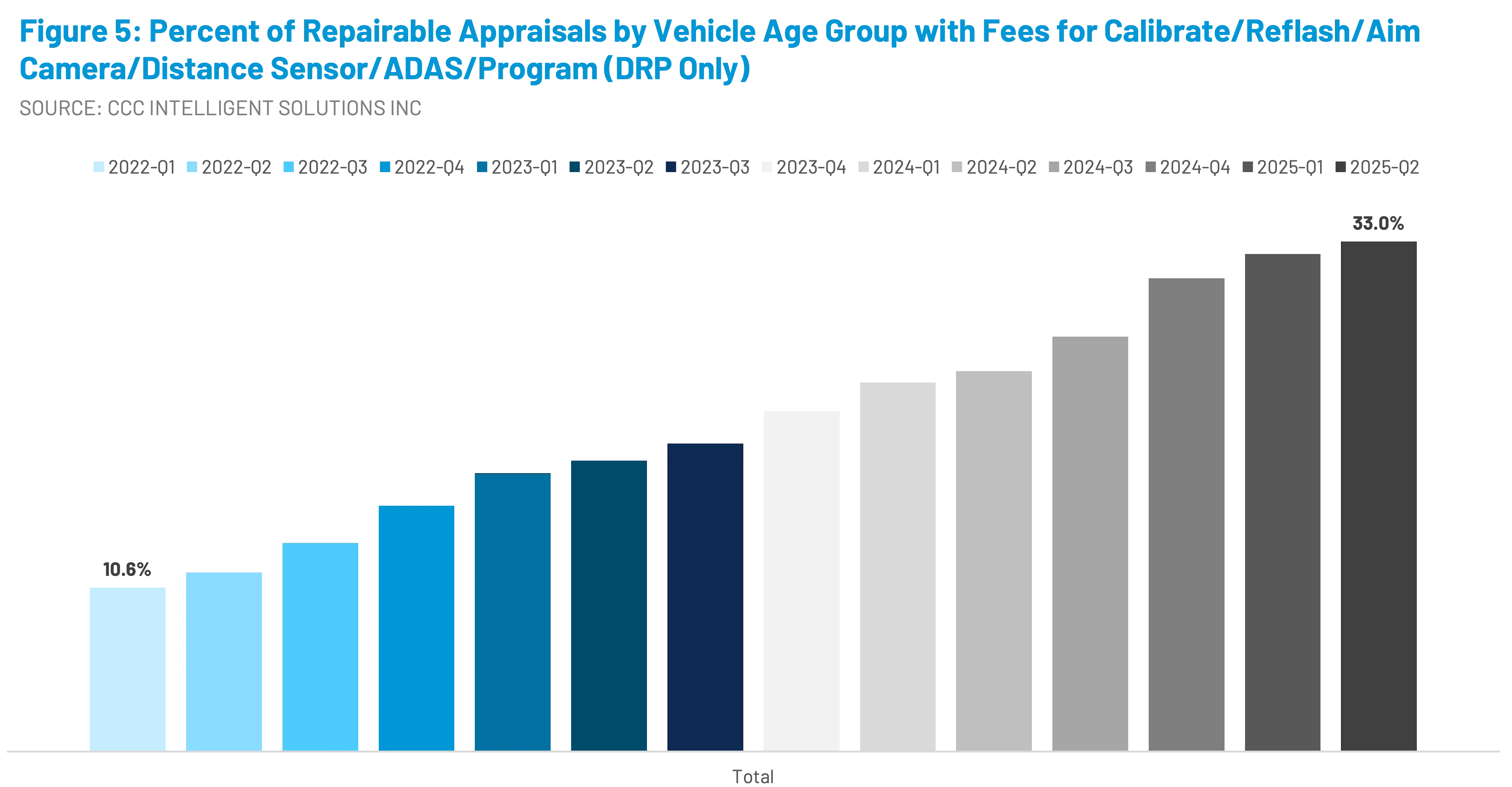

Fast forward to 2025, and the contrast is stark. Almost 70% of all repairable appraisals now include a scan, and more than 23% include a calibration. In DRP repairs specifically, those shares climb to nearly 86% and 33% respectively. (Figures 4 & 5)

This trajectory illustrates not only the rapid penetration of ADAS systems but also the industry's growing recognition of the critical role diagnostics play in making repairs safer and more complete.

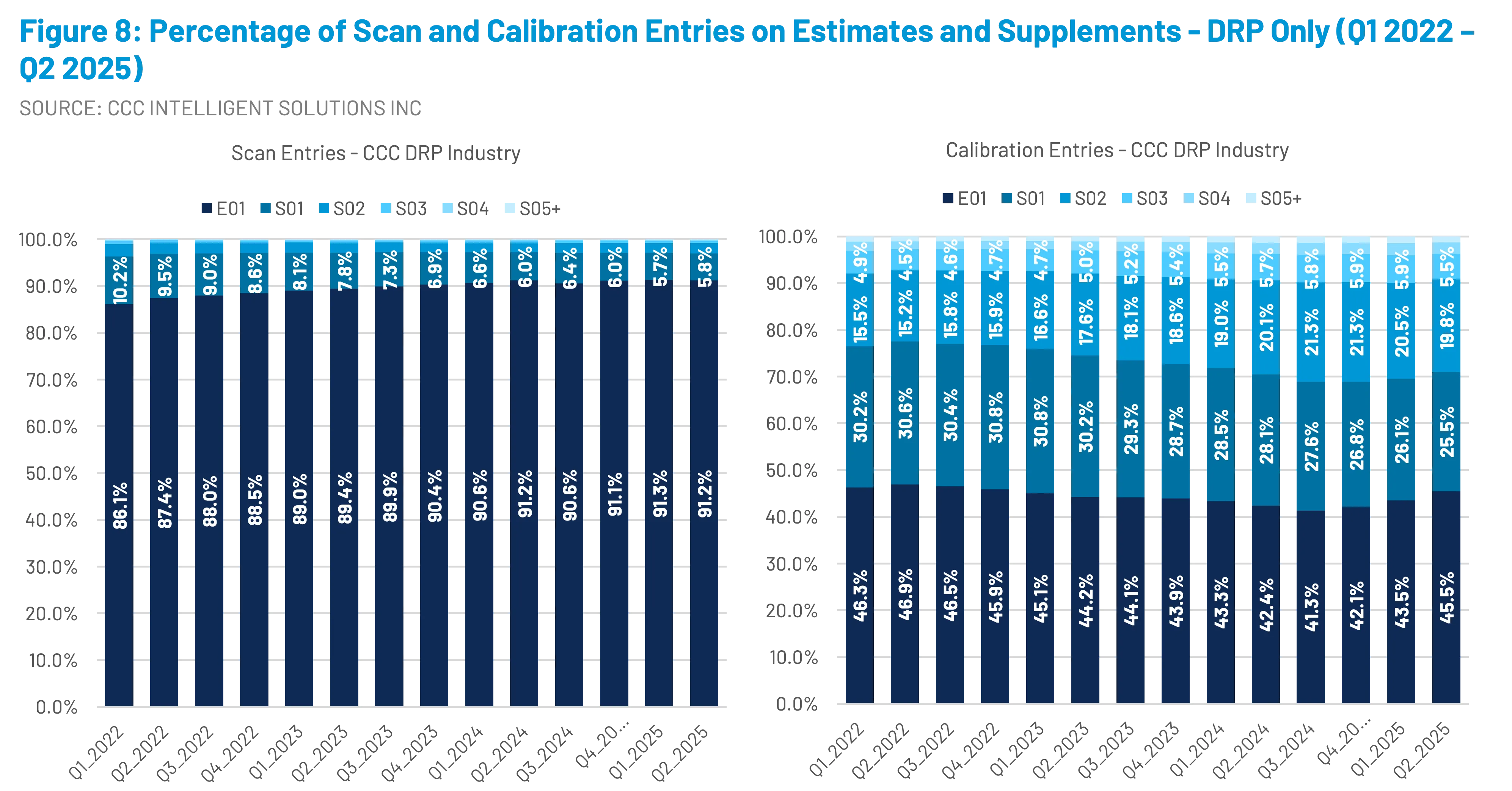

The data also highlights another critical development: while scans are almost always captured upfront on the initial estimate (more than 90% on the E01), calibrations lag behind. Less than 45% of calibrations are included on the first estimate; the majority emerge later as supplements. (See Figure 3)

This timing difference introduces downstream challenges – extended cycle times, customer frustration (especially when a vehicle needs to be returned to the shop and re-calibrated), and increased costs. These shifts tell a story of an industry racing to keep pace with technology. What began as an occasional procedure has become a daily necessity, with calibrations now representing one of the fastest-growing drivers of cost and complexity in auto repair.

More, Costlier Diagnostic Operations

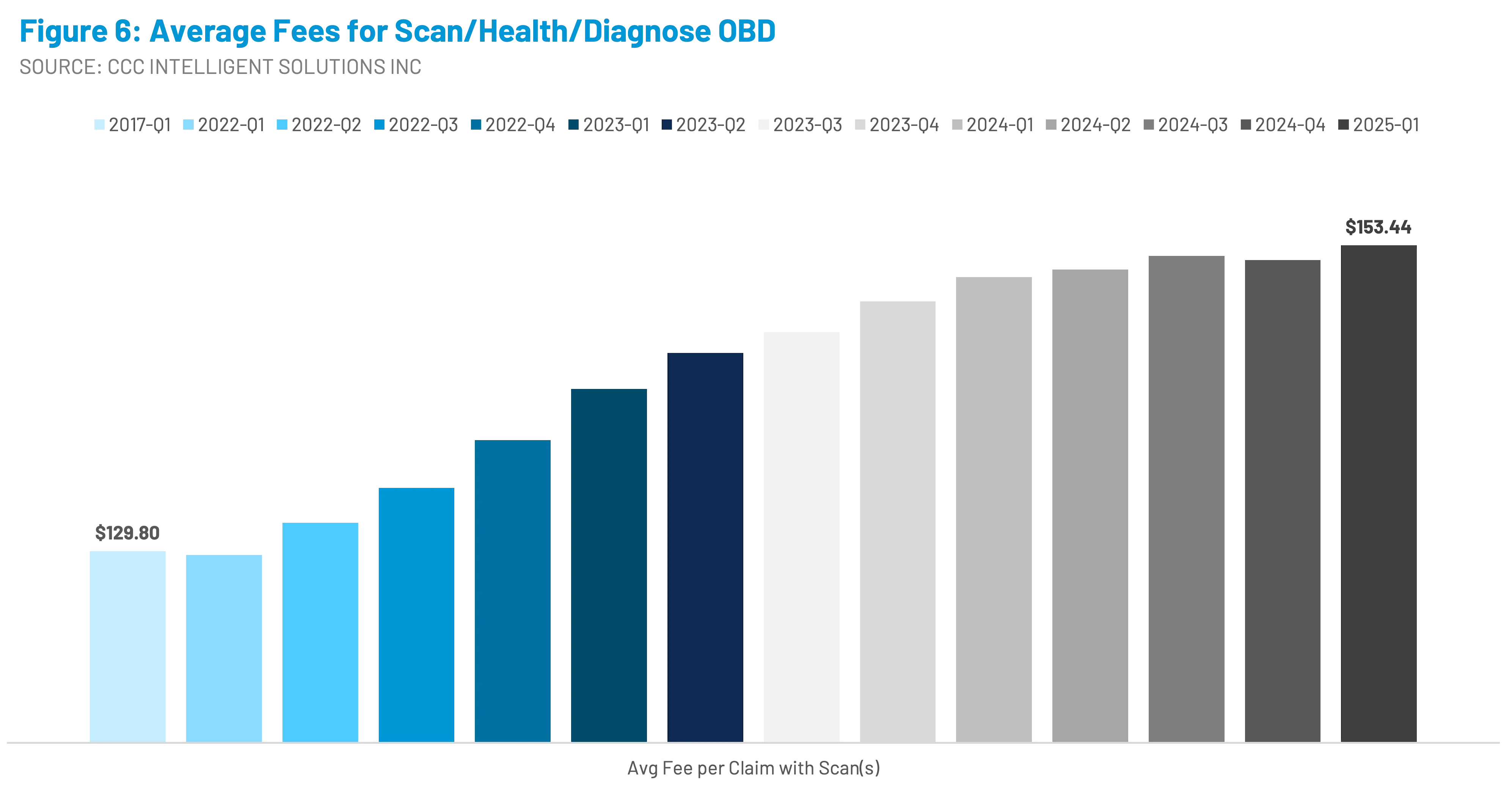

The financial picture has evolved just as dramatically. Between 2017 and 2025, average scan fees increased by roughly 18%, stabilizing in the $150 range over the last six quarters. (Figure 6)

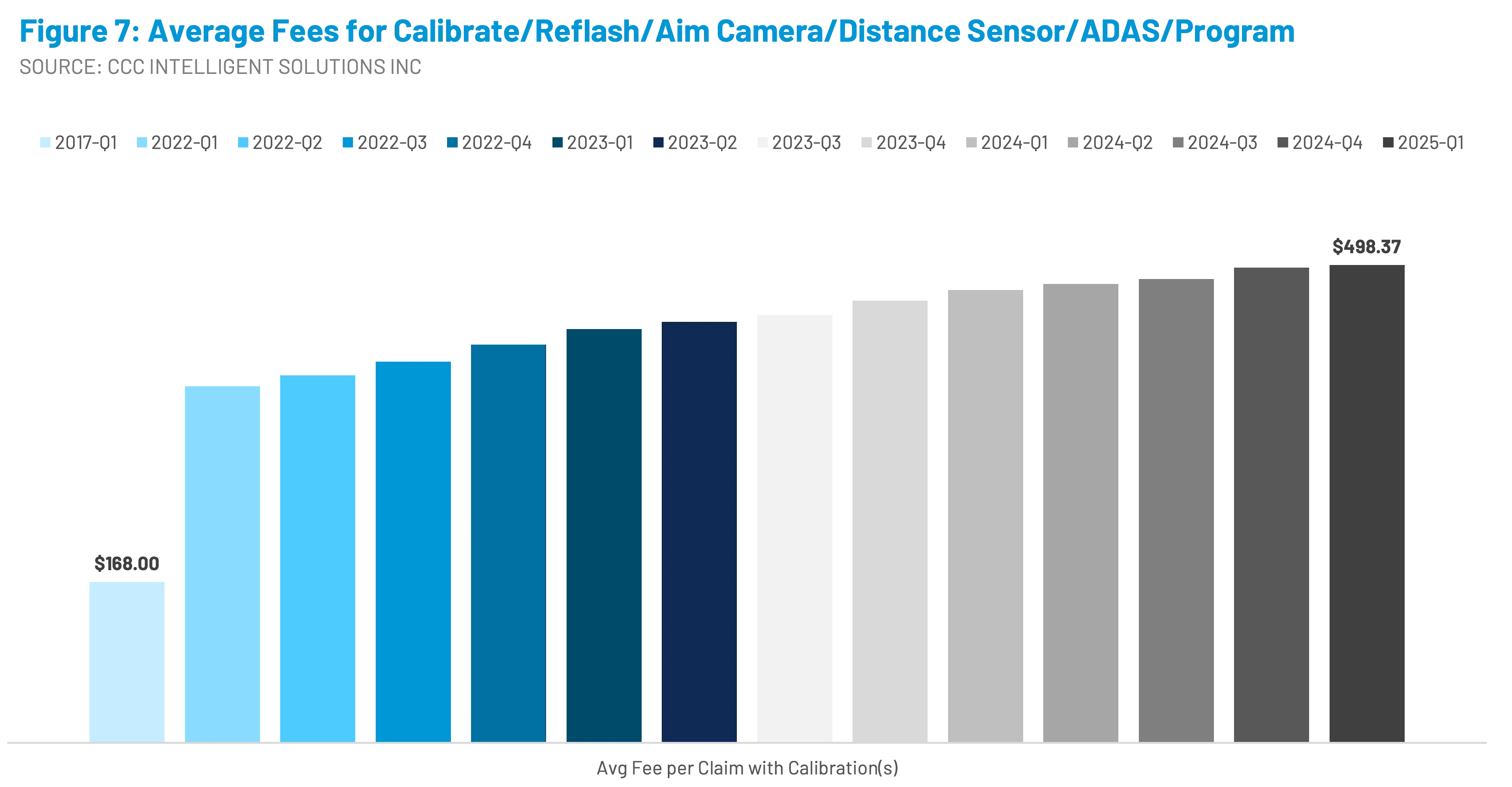

Calibration fees, by contrast, nearly doubled in just five years, reaching an average of $500 per vehicle. This escalation reflects many different factors including but not limited to; the increase in the number of calibrations performed per claim, the outsourcing of these services, the complexity of calibration procedures, and the specialized tools, training, and facilities required to perform them accurate. (Figure 7)

Many collision repair facilities do not yet have the in-house capability to complete every type of calibration due to the wide range of ADAS systems, each requiring proprietary tools, software access, and specialized training. This creates a complicated web of requirements and expense that can be difficult for even large MSOs to fully support.

As a result, subletting calibrations to vendors or OEM dealerships has become a common practice. For some shops, this means working with mobile diagnostic providers who travel to the repair facility and complete calibrations on-site. For others, it requires physically moving the vehicle to a dealership or third-party vendor equipped with the necessary factory tools. Both approaches carry additional costs and potentially extend cycle times. The reliance on sublets also introduces logistical friction: vehicles may sit idle waiting for scheduling, transportation, or vendor availability.

For insurers and policyholders, this creates variability, as calibrations performed in-house will differ from calibrations performed at a dealership in both turnaround time and pricing.

Current Adoption Trends

The adoption of calibrations has followed a steep upward curve, driven by the accelerating penetration of ADAS across the U.S. vehicle fleet. In Q2 2025 alone, 33% of repairable DRP appraisals included a calibration – up over eight percentage points from Q2 2024. (See Figure 3)

This growth is significant for two reasons. First, it underscores the inevitability of calibrations becoming a required component of most repairs, especially as newer vehicles with more sensors enter circulation. Second, it reveals a widening gap between how scans and calibrations are managed within the repair process.

While 91.2% of DRP scans appeared on the initial estimate in Q2 2025, just 45.5% of calibrations were captured there. The remaining 54.5% were added later as supplements. (Figure 8)

The problem with adding calibrations to supplements is that it can delay repair cycle times and inflate costs, especially for shops using sublet vendors and even those with in-house capabilities, as they have to re-perform procedures once the need is identified.

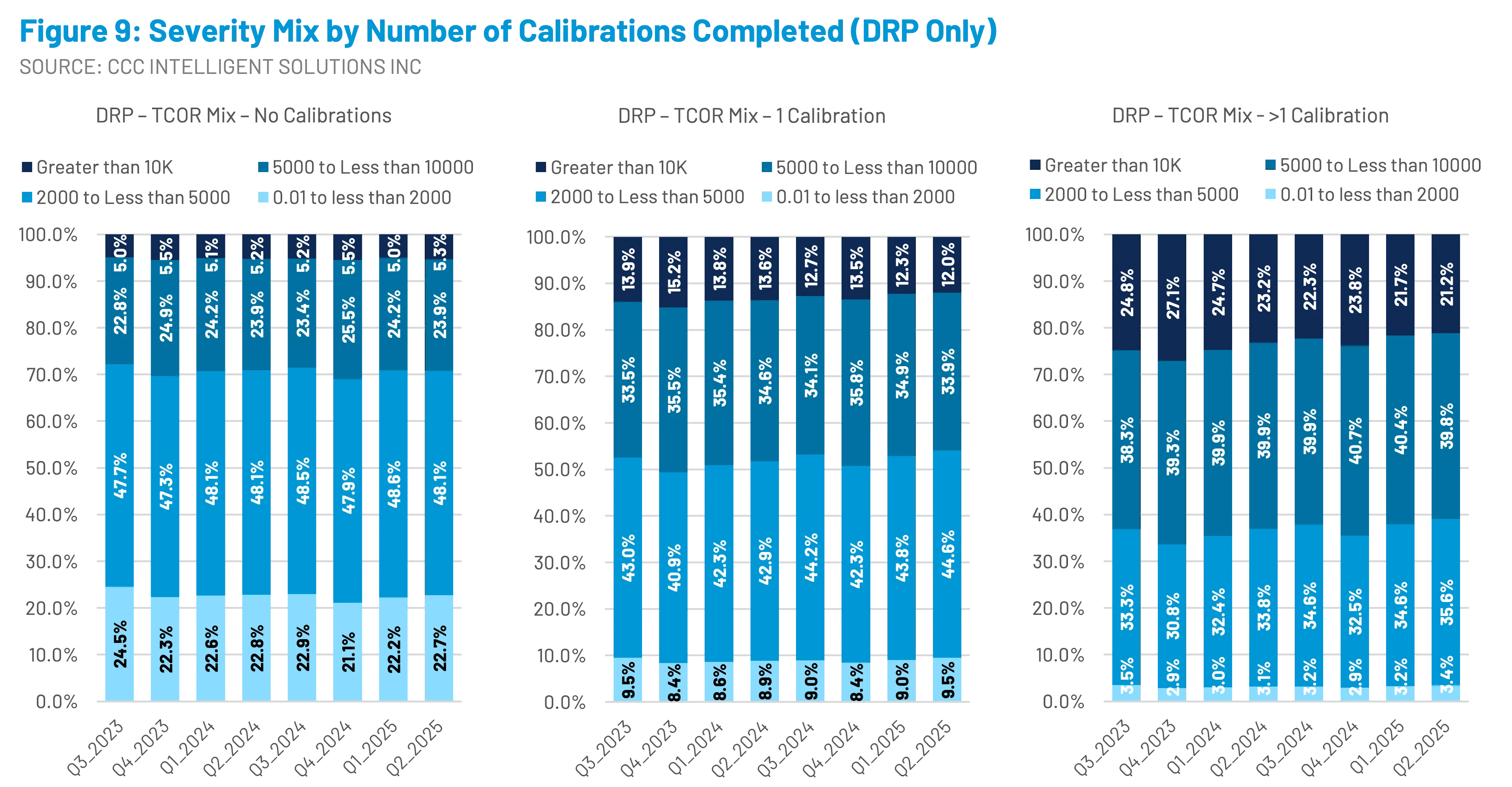

The prevalence of calibrations is also reshaping the repair mix. Industry data reveals that claims including calibrations are less likely to fall into lower-cost categories. Repairs under $2,000, once a sizable share of DRP repairable claims volume, shrink dramatically when calibrations are involved. With one calibration, fewer than 10% of DRP repairs fall below the $2,000 threshold; with multiple calibrations, that figure drops to just 3%. (Figure 9)

This trend signals a long-term structural shift. As ADAS-equipped vehicles dominate the car parc, low-dollar claims will become increasingly rare, replaced by higher-cost repairs. For insurers, this means resetting expectations around severity and supplement frequency. For repairers, it means building the capacity to deliver – and properly document - complex, precise calibrations consistently.

Shops must weigh the investment required to bring calibrations in-house – including purchasing targets, alignment racks, and software licenses – against the flexibility and scalability of continuing to use sublet vendors. This balancing act will likely continue to shape how calibration fees trend in the years ahead.

Cost Implications on TCOR

The rising prevalence of calibrations is closely tied to another industry-wide trend: the steady increase in the total cost of repair (TCOR). While labor rates, parts prices, and supply chain dynamics all contribute to rising costs, calibrations are a growing slice of the pie.

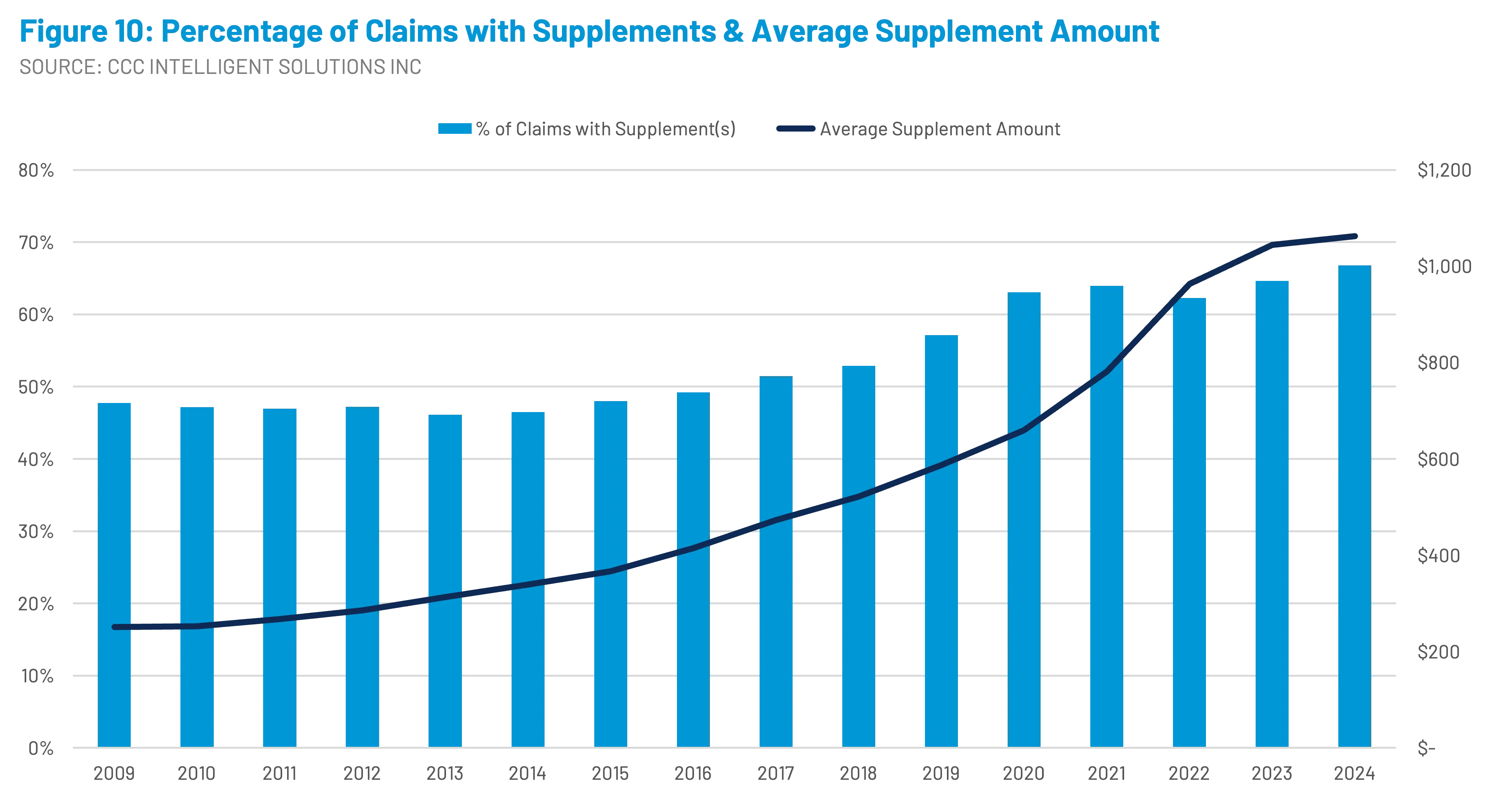

Between 2009 and 2024, the average supplement increased more than fourfold, from around $250 to over $1,060. (Figure 10)

Much of this growth stems from vehicle complexity, including the need for diagnostic scans and calibrations. Unlike cosmetic repairs, calibrations are not discretionary — they are required to restore safety-critical systems to OEM standards.

The financial weight of calibrations shows up clearly in claim distributions. For DRP repairs with no calibrations, nearly 70% of repairs cost less than $5,000. Add a single calibration, and that share drops to about 50%. Add more than one, and fewer than 40% of repairs remain under $5,000.

The decline is even sharper in the lowest-cost bracket. Repairs under $2,000 make up about 22–23% of DRP claims without calibrations. With one calibration, that shrinks to less than 10%. With multiple calibrations, it collapses to just 3%. These shifts not only elevate average severity but also reshape the economics of collision repair. (See Figure 3)

The fee structure magnifies the impact. With calibrations averaging $500 per claim, even a single procedure can meaningfully alter claim severity. And because calibrations often occur in tandem with other repairs – such as windshield replacement or bumper repair – their costs layer onto already-expensive parts and labor.

From an insurer's perspective, calibrations add both predictability and unpredictability. The per-procedure fee is relatively standardized, but the timing of when calibrations appear (E01 vs. supplement) introduces variance into the claim. This duality underscores the importance of standardizing calibration costs and improving calibration identification and documentation upfront, thus reducing reliance on supplements to capture them later.

From a strategic standpoint, this has two major implications:

- Insurers should consider recalibrating internal forecasting and reserve planning to reflect the declining share of low-dollar claims and the growing influence of vehicle ADAS features on repair requirements.

- Repairers should consider adapting their operations to handle a higher concentration of mid- to high-severity repairs, and provide their teams with the resources they need to estimate, document and repair in the most efficient manner possible

Cycle Time Impact

Cycle time – the number of days from when a vehicle enters the shop to when it leaves – is another area where calibrations exert outsized influence.

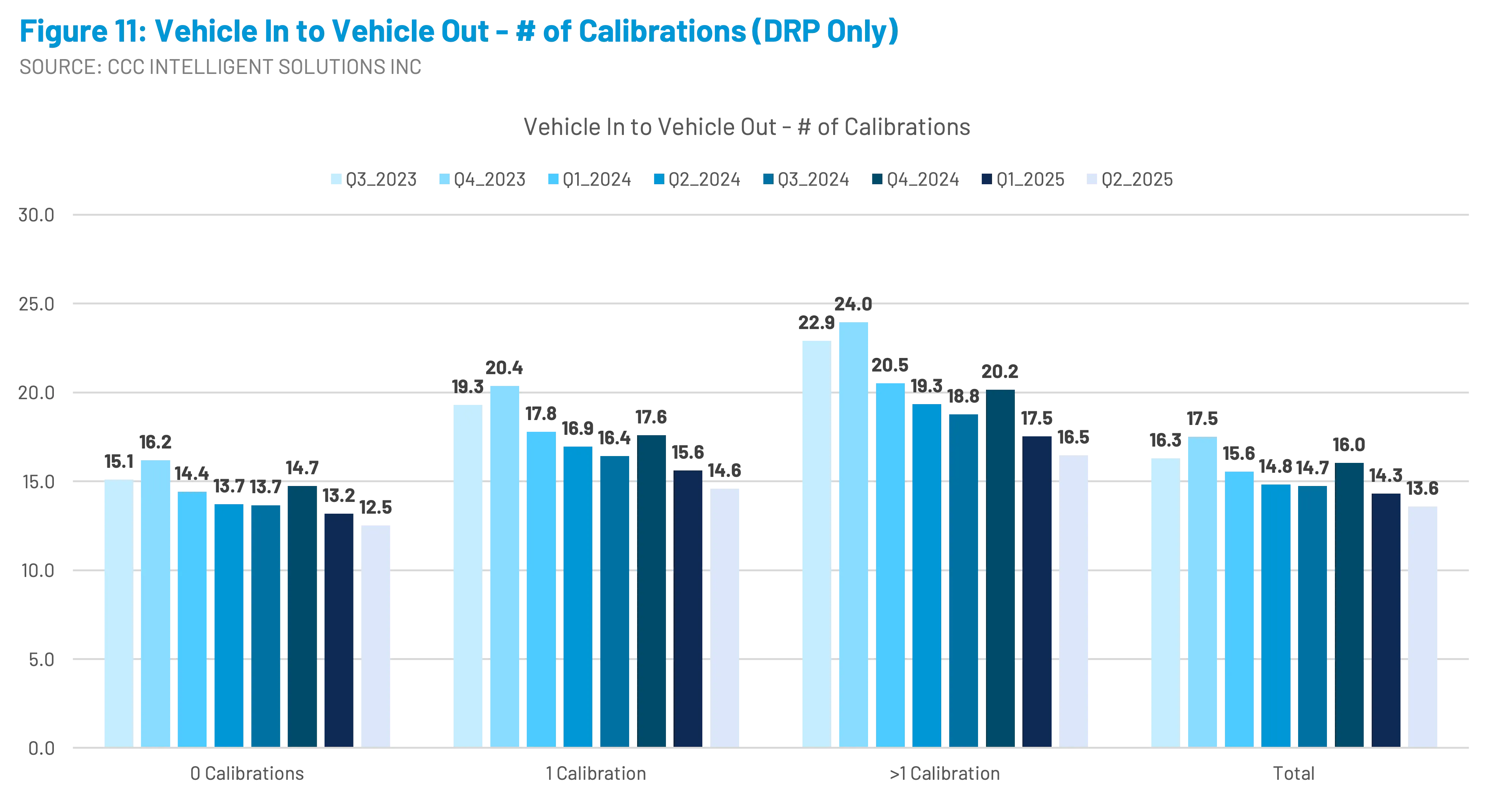

In 2024, DRP claims requiring one calibration took about 20% longer to complete, adding roughly three days. Those requiring more than one calibration took nearly 40% longer, adding 5.5 days. (Figure 11)

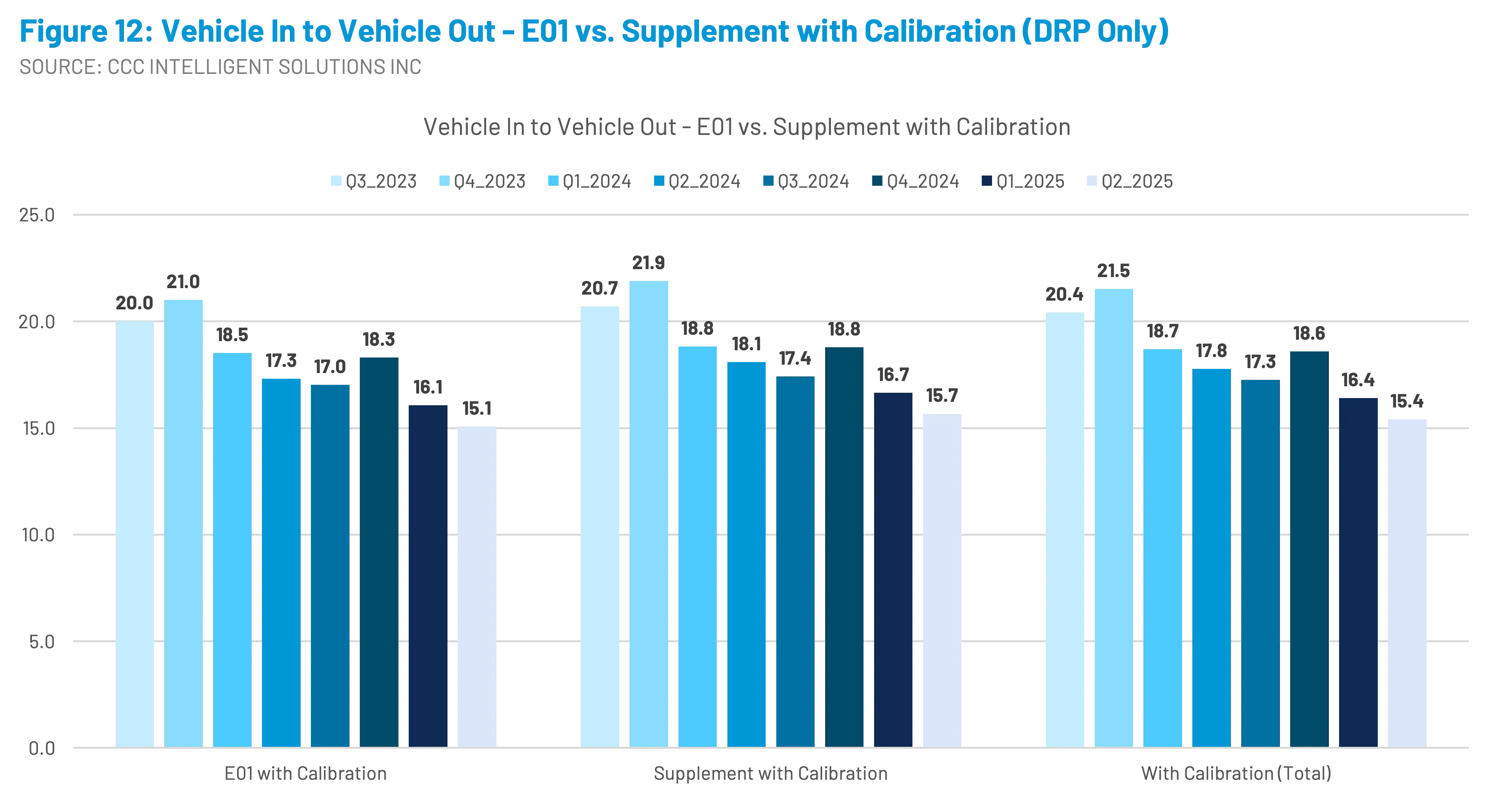

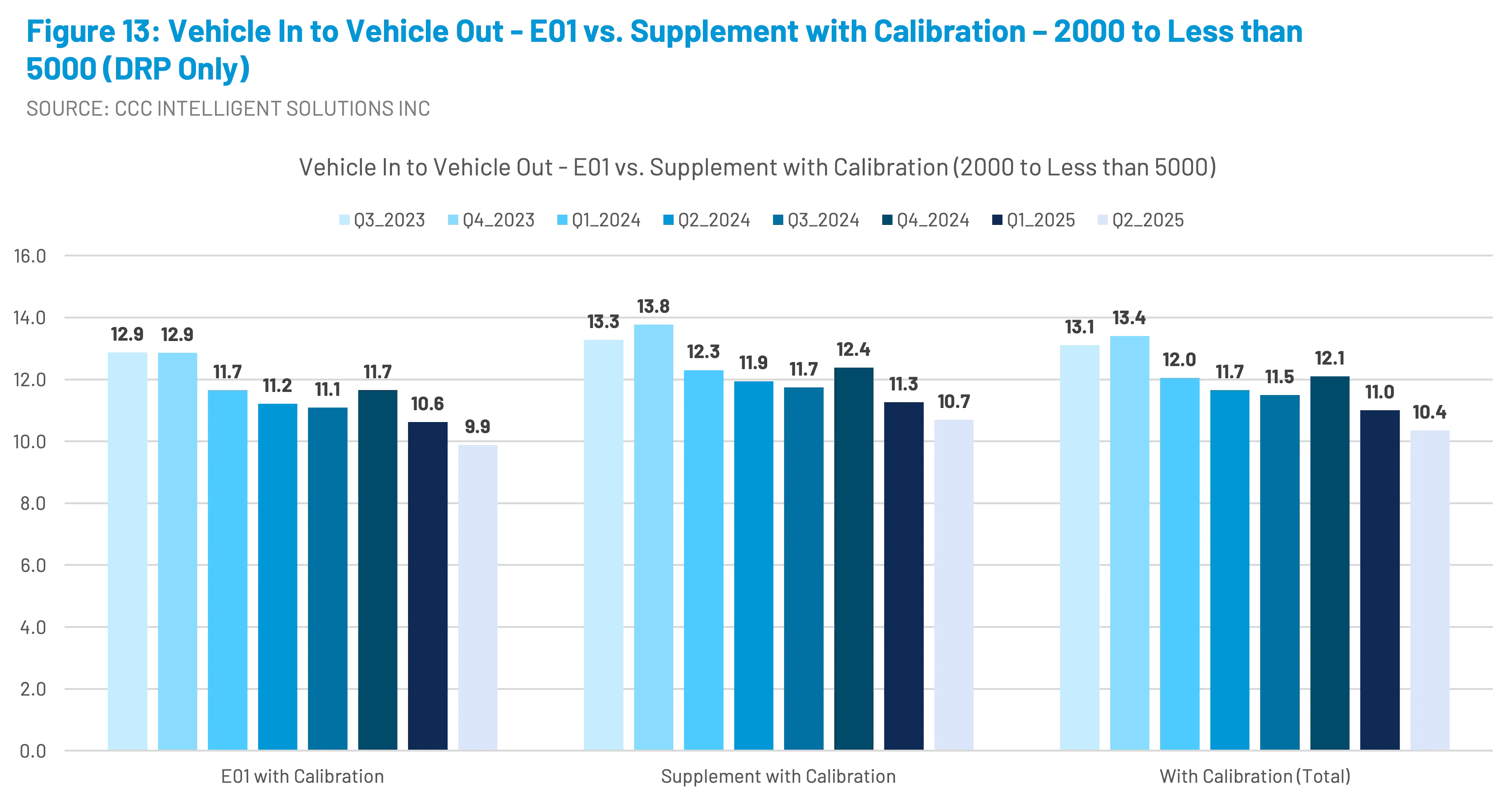

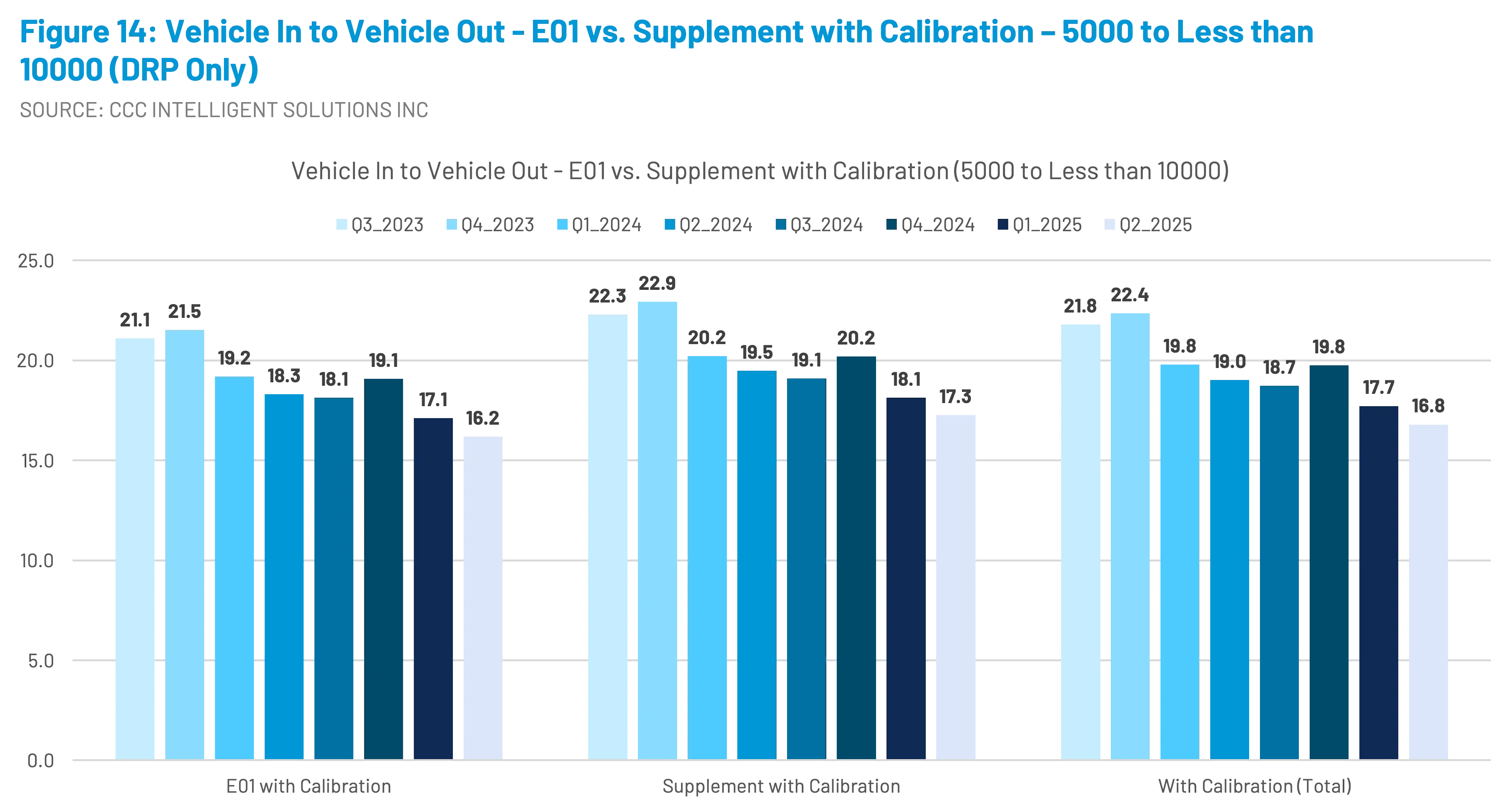

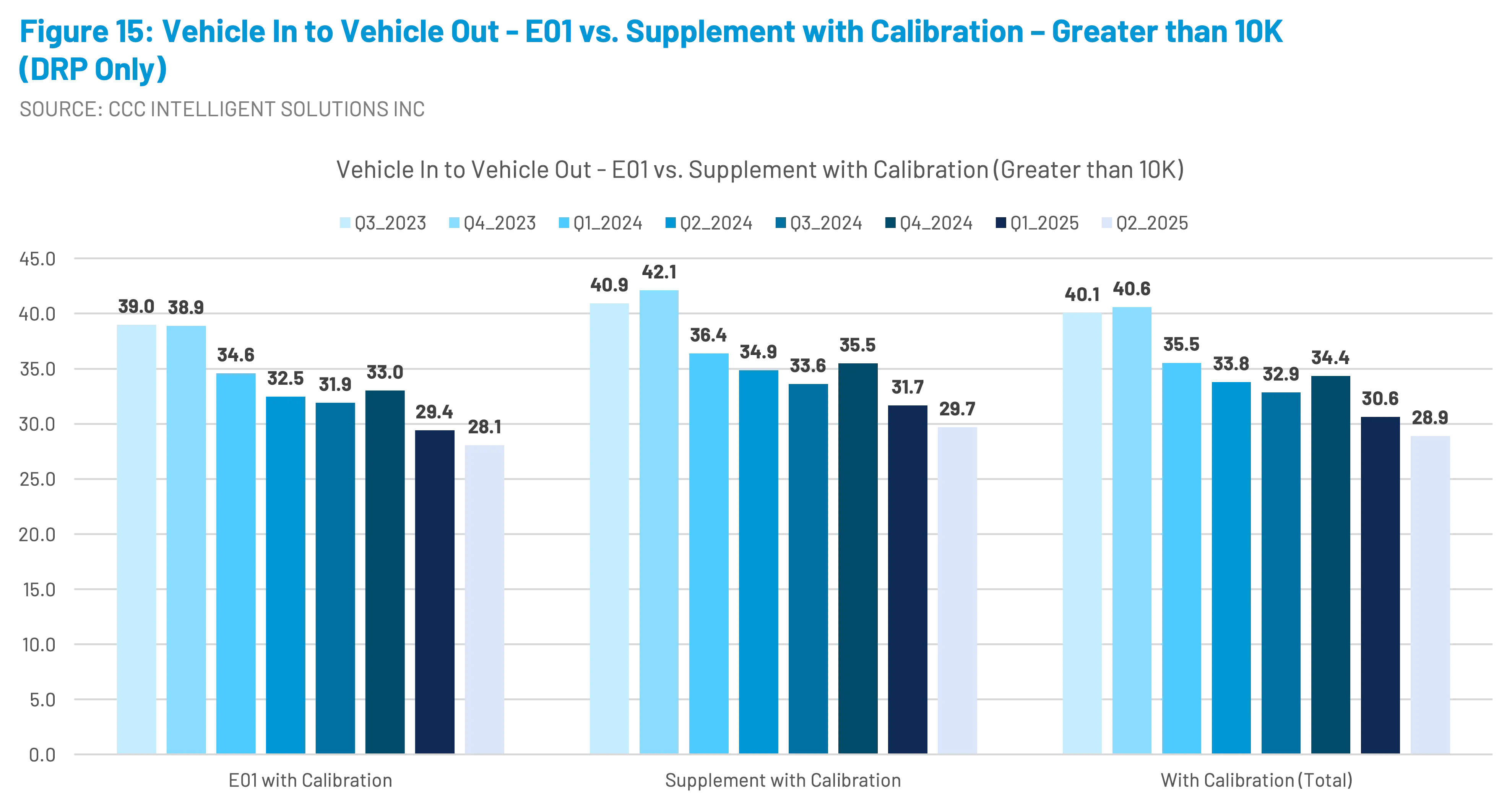

This impact is magnified when calibrations appear as supplements. Data from Q2 2025 shows that repairs where calibrations are included on the initial estimate (E01) are, on average, completed about half a day faster than those where calibrations are added later. (Figure 12)

The time savings increase with repair severity. For example:

- $2,000–<$5,000 repairs: 0.8 days saved when calibrations are captured upfront (Figure 13)

- $5,000–<$10,000 repairs: over one full day saved (Figure 14)

- >$10,000 repairs: over a day-and-a-half saved (Figure 15)

This pattern highlights the operational importance of identifying calibration needs early. When calibration needs aren’t caught early, shops must pause the repair, schedule new procedures, and often wait for additional approvals – each step extending the repair timeline.

For customers, these delays can translate to extended rentals as they spend more time without their vehicles, which then leads to inflated claims costs for insurers. For repairers, these longer cycle times tie up bays and reduce throughput. This is why capturing calibrations on the initial estimate or during disassembly while repair planning is best practices and a critical lever for improving efficiency and customer satisfaction.

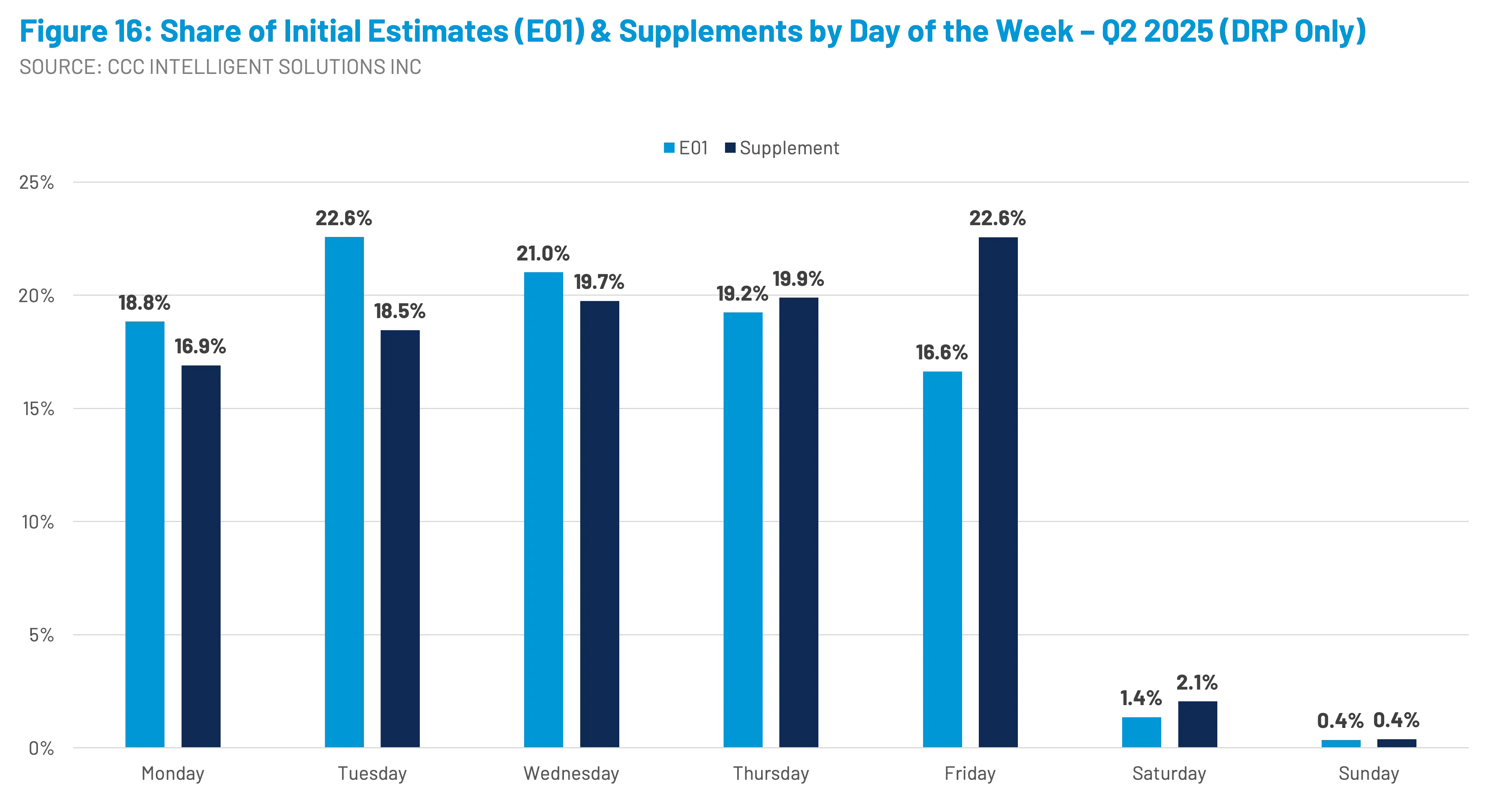

A new analysis of when initial estimates and supplements are completed by appraisers indicates that the distribution of initial estimates (E01) generally falls early-to-mid week, peaking on Tuesdays and decreasing through the end of the week. Supplements, however, increase as the week develops, with the largest share of supplements being completed on Fridays. Supplements generally require review and approval when associated with a claim, meaning that there is a higher probability of vehicles sitting over the weekend, further aggravating cycle times and rental expenses. (Figure 16)

ADAS Proliferation and the Road Ahead

The trajectory of calibrations is directly tied to the spread of ADAS technologies.

Projections from IIHS/HLDI underscore the scale of the shift. By 2029, approximately 78% of registered vehicles will have rear cameras, 55% will have front automatic emergency braking, and over 56% will feature lane departure and/or blind-spot monitoring systems.

In contrast, more advanced features like adaptive cruise control with lane centering (25%) and curve-adaptive headlights (16%) will remain less common. (See Figure 1)

Still, the trend line is unmistakable: more sensors, more systems, more complexity.

As these features become standard, the frequency of calibrations will continue to rise. Today’s 32% calibration share in DRP claims is likely a waypoint, not a plateau. Within a few years, calibrations could be required in the majority of repairs, fundamentally altering the economics and workflows of collision repair.

Operational and Strategic Implications

The rise of calibrations presents challenges and opportunities across the ecosystem:

- For repairers: Investments in equipment, training, documentation, and partnerships are essential to manage consumer and insurer expectations and deliver quality, timely repairs. Shops must decide whether to perform calibrations in-house or rely on sublet vendors, balancing cost, convenience, and liability.

- For insurers: Accurate estimating and timely supplement review are critical as calibrations increasingly appear mid-repair. Encouraging shops to identify calibrations on the E01 reduces supplement frequency and cycle time, while thorough documentation – including scan reports, OEM procedures, and vendor invoices – increasing accuracy, compliance, and faster claim resolution. Carriers must also prepare for higher average severity and fewer low-dollar claims.

- For OEMs: The proliferation of ADAS creates a dual responsibility – designing systems that improve safety while ensuring they can be efficiently serviced post-collision. Clear repair procedures and diagnostic requirements are critical to industry adoption.

- For customers: The expectations are shifting. Longer cycle times and higher repair costs may frustrate policyholders, but transparency and education can help them understand the safety-critical importance of calibrations.

Final Thoughts

The calibration era is here, reshaping nearly every facet of auto repair. What was once a specialized diagnostic step has become a core element of restoring today’s increasingly complex vehicles.

As ADAS technologies proliferate, calibrations will only become more routine and more consequential. The industry must adapt to a reality where precision, documentation, and collaboration matter as much as speed and cost control.

Adapting to the influx of calibrations will require more standardization across the entire auto claims and repair ecosystem – shops must expand capabilities, insurers must prioritize accuracy in estimating and supplements, and OEMs must continue to provide clear procedures to make sure every repaired vehicle isn’t just visually complete, but functionally safe and road-ready.