Click here to receive monthly CCC Trends reports and other insights

Electric vehicles (EVs) have become an undeniable catalyst for change in the automotive industry as they continue to grow in popularity and market share. With approximately two million currently on the road, accounting for about 1% of all vehicles in operation, the current EV market share may seem relatively modest; however, the future paints a different picture as EVs are projected to capture anywhere from 30% to 50% of new car sales globally by 2030.

This optimistic outlook is underpinned by growing environmental consciousness, the rapid expansion of charging infrastructure, competitive pricing expected to reduce cost, and now, government incentives aimed at amplifying these initiatives.

Legislation Supercharges EV Production

The Inflation Reduction Act (IRA) – the most significant climate legislation in U.S. history – includes a goal that requires EVs to make up 50% of all vehicles sold in the U.S. by 2030. Since the initial executive order was signed in August of 2022, the number of charging stations have doubled while EV sales have tripled. And last month, the Environmental Protection Agency (EPA) announced new emissions rules that are expected to force an EV market share of about 60% by 2030, and 67% by 2032.

Even if projections fall short, the rapid uptick in EV production – and subsequent adoption, which could take longer – will still require a massive investment in industry-wide transformation for the auto claims and collision repair segments, as organizations face a not-so-distant future in which a growing number of collisions will involve EVs.

Given the forecast, what can auto claims and collision repair organizations do to prepare for the changes and opportunities ahead? The following is an overview of current market trends to help inform how you can effectively manage rapid EV adoption.Note: Data below is based on Battery Electric Vehicle (EV).

Not included is data on PHEV (Plug-In Hybrid Electric Vehicle), FCEV (Fuel Cell Electric Vehicle), or HEV (Hybrid Electric Vehicle).

EV Crash Trends

In a recent E-Vision Intelligence Report, J.D. Power showed an increase in consumers who were “very unlikely” to consider purchasing an EV. The top contributing factors were tied to charging station infrastructure and availability, affordability, vehicle range, and charging time, but only 21% cited a lack of available and/or capable repair centers (Figure 1).

This lack of consideration for EV repair and corresponding casualties could be a blind spot. Though many EVs are designed with ADAS and other safety features and undergo the same rigorous Federal Motor Vehicle Safety Standards testing as other light duty cars and trucks in the U.S., there can be a steep learning curve when it comes to driving them safely.

A survey of 1,200 EV owners conducted by the French insurer AXA in Belgium revealed drivers of EVs caused 50% more collisions than ICE vehicles. Drivers switching from an ICE vehicle to EV are often unaware of how quickly an EV accelerates, and the high, instant torque of electric motors can lead to loss of control which can result in a crash.

Many of the EV models being introduced are high-performance vehicles – they accelerate as fast as supercars but cost far less, and early data suggests EV drivers have more accidents. Though the added weight in EV and hybrid vehicles means passengers are less likely to be injured in a crash than those in similar gas-powered vehicles, this can be bad news for other vehicles and their occupants when hit, as the added impact force is transferred to the other, lighter vehicle.

It also stands to reason that EVs traveling at higher speeds will produce even greater impact force, resulting in more damage, higher claims costs, and longer cycle times. Also contributing to growing claims costs is the higher MSRPs for EVs. Nearly 50% of EV claims in 2022 comprised vehicles with original MSRPs greater than $50K (Figure 2).

The handling of damaged EV parts after a collision can also be complex, requiring assistance from specific organizations like The Energy Security Agency to safely dispose or transport EV parts and materials from the scene of the loss until it’s returned to the customer or salvaged. This complex process requires special considerations, such as:

- Intermittent battery charging and charge level monitoring

- Vehicle storage and distancing

- Scan and calibration procedures; and

- Data management (in cases of a total loss.)

EV repair and maintenance can have far-reaching implications for claims organizations and collision repair shops that are not being adequately addressed from a legislation and funding perspective, particularly when it comes to technical training and development.

EV Claims Trends

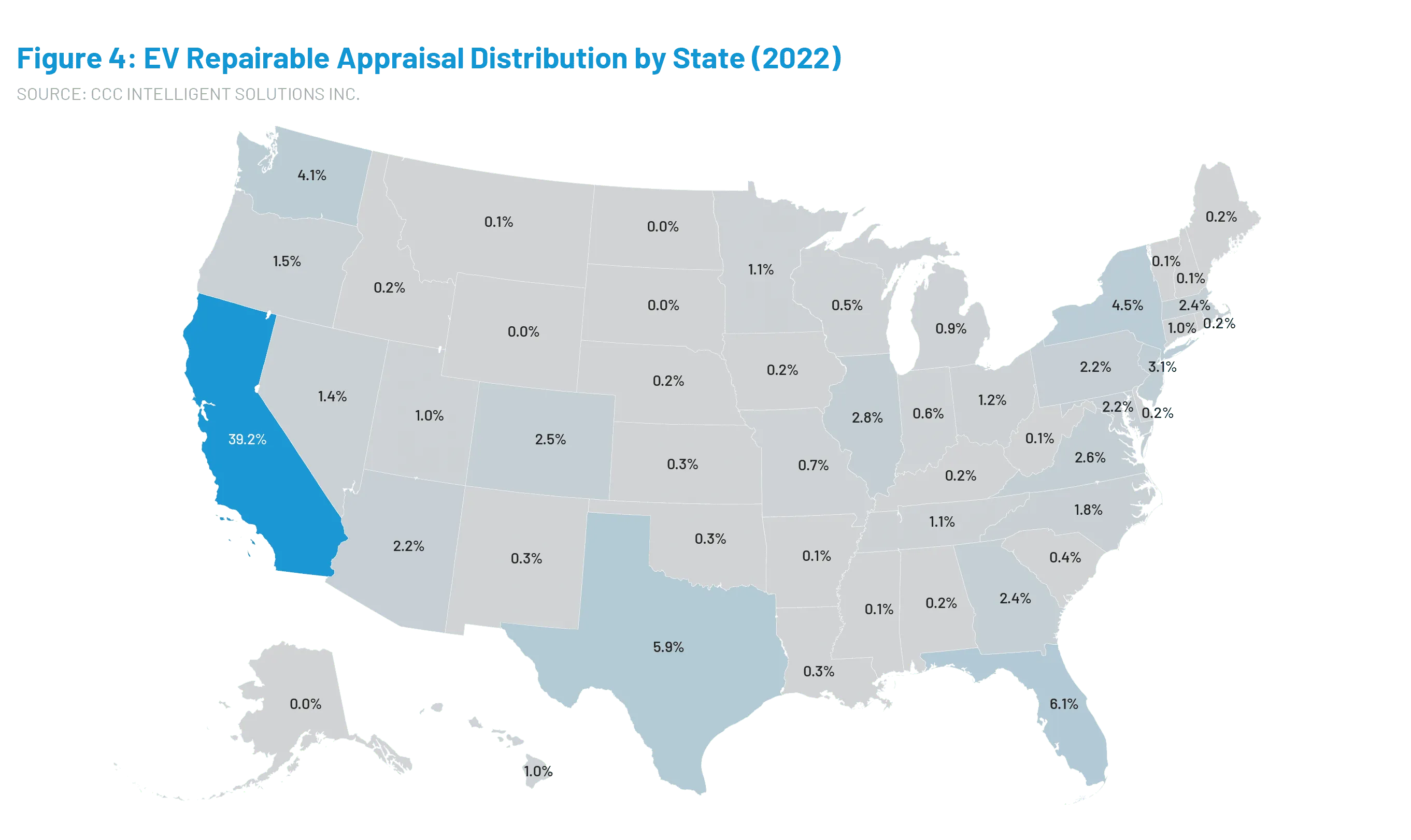

In 2022, EVs represented 1.2% of all repairable estimates processed through CCC – a 96% increase from 2021 (Figure 3). Over 39% of estimates in 2022 were from California, a state that represents 40% of all U.S. EV sales since 2011, with San Francisco recently becoming the first U.S. region to hit a 50% EV adoption rate. But outside of California, EV sales have been greatest in Florida, Texas, Washington, New York, and New Jersey. CCC’s estimating results are largely correlated to those sales trends (Figure 4).

The U.S. EV market is currently dominated by Tesla, which accounted for ~65% of all new EV sales in 2022. Tesla’s consistent position as the U.S. EV market leader is reflected in 2022 numbers, representing 78.6% of CCC repairable estimates (Figure 5). Nissan, Chevrolet, Ford, Hyundai, Kia, Volkswagen, Audi, and BMW comprised the next tranche of auto brands – all representing between 1-4% of 2022 estimates, respectively (Figure 6).

In 2022, electric native manufacturers accounted for 68.5% of new EV sales, with Tesla representing 94% and EV-only manufacturer sales. New entrants, such as Rivian, Polestar, Lucid, and Brightdrop, continue efforts to scale and market their offerings amidst the growing pool of EV brand and model options, which has led to fragmentation (Figure 7).

The fractured EV market is fundamentally changing the claims landscape, as electric natives introduce smaller quantities of new EV models and manage their life cycle from manufacturing, selling, and distributing to service and repair. The addition of “small batch” EV models – each with their own unique parts and systems – might require a more thoughtful approach when it comes to assessing EV risk, determining coverage, managing claims, and underwriting policies based on limited historic data, and could also present even bigger challenges that impact an already-strained collision repair industry.

EV Repair Trends

The average total cost of repair (TCOR) for EVs in 2022 reached $6,587 -- +56% compared to all non-EVs. This could be misleading as EVs are, on average, 4.5 years newer than the average vehicle estimated and have an average value that is over $30,000 greater (Figure 8). In comparing EVs to non-EVs by vehicle age, we still see TCORs that are +$1,211 for current year or newer and +$1,611 for 1- to 3-year-old EVs, and values that are $20,000 more than non-EVs (Figure 9).

This comparison revealed a few indications as to key drivers of EV TCOR differences. While non-drivable ratios and the percentage of claims with supplements are comparable to non-EVs (Figure 10), EV estimates average more than 15 additional lines on each appraisal (Figure 11).

An initial analysis revealed that EV estimates tend to include line items for parts, operations, and disposable goods that don’t typically appear on non-EV estimates. The average number of parts per estimate in 2022 for EVs was nearly double the number of parts per estimate for non-EVs. Parts costs account for ~30% of the TCOR difference between EVs and non-EVs (Figure 12), but the major driver of cost differences resides in labor, where EV non-paint labor time is over double the non-EV average and paint labor time is over 50% higher (Figures 13 & 14).

Labor costs also include specific operations that are required for safely storing and maintaining EVs while on premise, but not all repair technicians have the specialized training and continuing education necessary to do this. Some shops may account for the cost of this training and education and that consideration may be reflected in the pay offered to this new breed of collision technician. This reality, coupled with pervasive labor shortages, have contributed to longer cycle times for EV repair.

In 2022, the average time between last estimate and vehicle out was nearly 58 days, over 12 days more than non-EVs. Getting the vehicle into the shop added seven full days and repairs required an additional 5 days (Figure 15).

Capacity within the burgeoning network of certified EV shops appears to be the basis for longer cycle times, as well as the meticulous nature of procedures required to complete repairs. EV repair backlog is yet another consideration that remains unaccounted for in the proposed IRA bill.

EV Proliferation & Preparedness

Electric vehicles and the supporting ecosystem are in a transitory period, which makes EV preparedness even more challenging. At the same time, the potential to learn from blind spots and inform progress is also prevalent. The IRA and other EV infrastructure-supporting legislation and programs focus on EV production and consumer adoption; yet, these programs don’t seem to fully address the scale and broader ecosystem required to maintain and repair EVs, which will inevitably need servicing or repair.

The proliferation of EVs on America’s roadways will continue to exacerbate repair cycle times. In 2022, EVs took 25% longer just to get into a shop to begin repairs (see Figure 15) – already an indication of capacity issues with shops qualified to repair EVs. Without adequate funding, communication, and education, the burden to modernize repair facilities and train a new generation of collision and auto technicians could fall squarely on the shoulders of repair shops and dealerships. While this is not the biggest adoption-limiting concern compared to charging networks or range anxiety (see Figure 6), addressing the EV support network now before the system becomes overwhelmed will remain important.

Increasing awareness around the existing technician shortage and emerging need to support EV fleets might be the right place to start. Corresponding grants and funding – like those provided to scale EV adoption through the IRA – could be pursued at both local and national levels to enlist would-be technicians and modernize shops to perform work on EVs.

EV preparedness also raises the question of how insurance carriers are pricing, underwriting, and managing claims for these vehicles. As we have illustrated, EVs are different from ICE vehicles. Developing an understanding of the differences between EVs and non-EV counterparts can help carriers forge strategies to address this evolving market. Understanding elements such as towing, storage, charging and battery maintenance, as well as labor and parts cost considerations are also likely to improve expectations and results. EV owners may demand the same from their insurance provider.

A Look Ahead

The long-term implications of widespread EV adoption are varied. We know that legacy parts suppliers will have to make critical strategic decisions on how they plan to engage with EVs while continuing to support the combustion engine business. This is not a question of EVs alone but also the sustainability of the ICE industry -- will it inevitably be phased out? There may be a tipping point when ICE parts will begin to dry up, repair/replacement costs increase, and it may simply become too expensive to maintain this obsolete technology. This type of attrition could be a strong motivator for EV adoption.

With significant progress already made toward EV adoption given directives set forth in the IRA and regulations, auto claims and collision repair organizations have little time for complacency. These regulations have noticeable blind spots when it comes to EV claims processing, collision repair, and parts handling, which means the onus is on industry leaders to make short- and long-term improvements to support a burgeoning population of EV owners and drivers.